While traveling recently, I met an older couple who were living their retirement dream – exploring the world and joyfully proclaiming they were “spending their children’s inheritance.” Their laughter was infectious, but it made me think:

• Does it always have to be one or the other?

• Can we enjoy life to the fullest and leave a meaningful legacy?

The answer is yes.

For many, legacy planning means hoping there’s something left over for the next generation after death. But with a thoughtful strategy, you can plan for a vibrant, worry-free retirement and ensure you leave a meaningful legacy for your next generation.

A Case Study

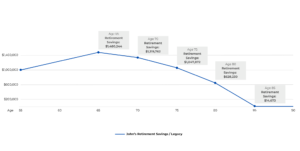

John, age 55, dreams of traveling the world with his wife Sarah and experiencing new cultures when he retires at age 65.

He plans to withdraw $60,000 annually (based on today’s value before accounting for inflation) from his savings, starting at age 65 and continuing until age 85 . With the help of his financial consultant, they determined that he would need a retirement savings of $1.48 million by the time he turns 65.

John also creates a Will to ensure that Sarah, along with his children Emily and Noah, will benefit in the event of his death.

But life is rarely that predictable. What if:

- John lives past 85 and require more funds?

- Unforeseen expenses, such as healthcare costs arise, leading to higher withdrawals?

- Can the legacy he leaves behind make a meaningful difference?

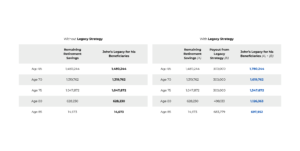

A Smarter Approach: Our Legacy Strategy

John explores a different path – diversifying $100,000 into our Legacy Strategy at age 55. Here is how it transforms his retirement and legacy:

Supplement for Retirement Needs

The Legacy Strategy allows John to tailor how he wants to grow his wealth with two distinct accounts. While he receives a consistent income stream from different sources of such as CPF Life, Supplementary Retirement Scheme (SRS) funds, insurance payout, and investment returns, he can withdrawal from the Legacy Strategy if needed.

A Meaningful Legacy

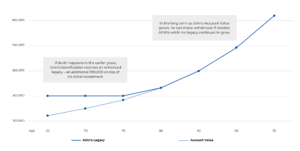

If death happens in the earlier years, John’s beneficiaries receive an enhanced legacy – an additional $200,000 on top of his initial investment of $100,000. In the long term, the account value of his Legacy Strategy grows, along with his legacy. This allows John to leave a meaningful inheritance for Emily and Noah, and even make an impact to causes he is passionate about.

With the Legacy Strategy, John can fulfil his retirement dream and also leave a meaningful legacy. He can live with peace of mind, knowing he has the resources to support both his life’s adventures and his family’s future.

Live More, Leave More

Your retirement should be a time to live more, not worry more. Let us help you align your financial future with your dreams and values.

Click the “Contact Me” button below for a complimentary consultation and discover how our Legacy Strategy can help you live the life you want.