My mom was diagnosed with early-stage cancer three years ago.

The doctor’s first words after “we caught it early” were about treatment timelines. Radiotherapy. Chemotherapy cycles. Follow-up scans. Medication schedules.

The hospital bill estimate came later. Insurance would cover most of it. We’d manage the co-payment.

What nobody prepared us for was the calendar. Six months where normal life stopped. Thirty radiotherapy sessions. Bi-weekly specialist appointments. Unpredictable recovery days when side effects hit hard.

The bills were covered. The time wasn’t.

This is what I wish someone had told us before treatment started.

What Early-Stage Cancer Treatment Actually Looks Like in Singapore

Early-stage cancer sounds manageable. Caught early, survival rates are high. Treatment is effective. The prognosis is good.

But “manageable” doesn’t mean “quick.”

Here’s what a typical early-stage cancer treatment schedule looks like in Singapore’s public healthcare system:

Radiotherapy Schedule

Standard protocol: 5 days per week, 6-7 weeks Total sessions: 25-35 sessions Time per session: 15-30 minutes treatment + 30-60 minutes travel and waiting Total time commitment: 30-50 hours over 6-7 weeks, not including travel

Reality: You’re going to the hospital 25-35 times. If you work full-time, that’s 25-35 times you need to leave work, adjust your schedule, or take time off.

Note: Some newer breast cancer protocols offer shortened courses of 1-2 weeks for suitable patients, but conventional fractionation remains standard for many cancer types.

Chemotherapy Cycles (if prescribed)

Typical cycle: Every 2-3 weeks for 3-6 months Sessions: 4-8 cycles Time per session: 2-6 hours (depending on drug protocol) Recovery days: 3-7 days post-treatment where side effects peak

Reality: Each cycle means a full day at the hospital plus several days of reduced capacity. If you’re the patient, you can’t work those days. If you’re the caregiver, you’re taking time off too.

Specialist Appointments

Frequency during active treatment: Every 2-3 weeks Frequency post-treatment (first year): Every 1-3 monthsTime per appointment: 1-3 hours (waiting + consultation + pharmacy)

Reality: Even after active treatment ends, you’re at the hospital every 1-3 months for the first year. That’s 4-12 appointments. Each one takes half a day minimum.

Imaging and Lab Work

During treatment: Weekly to bi-weekly blood tests, periodic scans Post-treatment: CT/MRI scans every 3-6 months for the first 2 years

Reality: More hospital trips. More time away from work. More schedule disruption.

The Income Gap: When Work Hours Drop

Hospital insurance covers treatment costs. But it doesn’t replace income when you can’t work full-time.

Scenario: Full-Time Employee with Early-Stage Cancer

Monthly income: $6,000 Monthly expenses: $5,000 (mortgage, utilities, childcare, parent support)

Treatment period: 6 months Work disruption: Frequent appointments, recovery days, reduced capacity

Typical patterns observed:

- Treatment days require full-day or half-day absence

- Recovery days following chemotherapy may require 3-7 days off

- Ongoing fatigue may reduce work hours or productivity

- Annual leave exhausts quickly in first 2-3 months

Income impact examples:

- If 40-60 days of work missed over 6 months

- Annual leave covers 14-21 days

- Remaining 20-40 days may be unpaid leave

- Estimated lost income: $4,000-8,000 over 6 months

If you’re the caregiver:

- Additional leave needed for appointments and support

- May require 20-30 days over treatment period

- If exceeding annual leave: additional $3,000-6,000 lost income

Combined household impact: $7,000-14,000 over treatment period

And this assumes:

- Employer allows flexible leave

- Job is secure during treatment

- You can return to full capacity after 6 months

Not everyone has these circumstances.

The Caregiver Time Cost

If you’re not the patient, you’re probably the caregiver. And caregiver time has a cost.

Estimated Time Investment for Primary Caregiver (6-month treatment period):

Transport to/from appointments: 70-85 trips × 2-4 hours = 140-340 hours Waiting at appointments: 70-85 visits × 1-2 hours = 70-170 hours Managing medications: 30 mins/day × 180 days = 90 hours Meal prep for recovery days: 1 hour/day × 60 days = 60 hours Emotional support and coordination: Substantial but variable

Estimated total caregiver time: 360-660 hours over 6 months That’s equivalent to: 9-16 full work weeks

Cost implications:

- If taking unpaid leave: At $25/hour average wage, that’s approximately $9,000-16,500 in lost income

- If hiring help: Home care services typically cost $2,500-4,000/month

Note: These are illustrative estimates. Actual caregiver time varies significantly based on patient needs, family support availability, and treatment intensity.

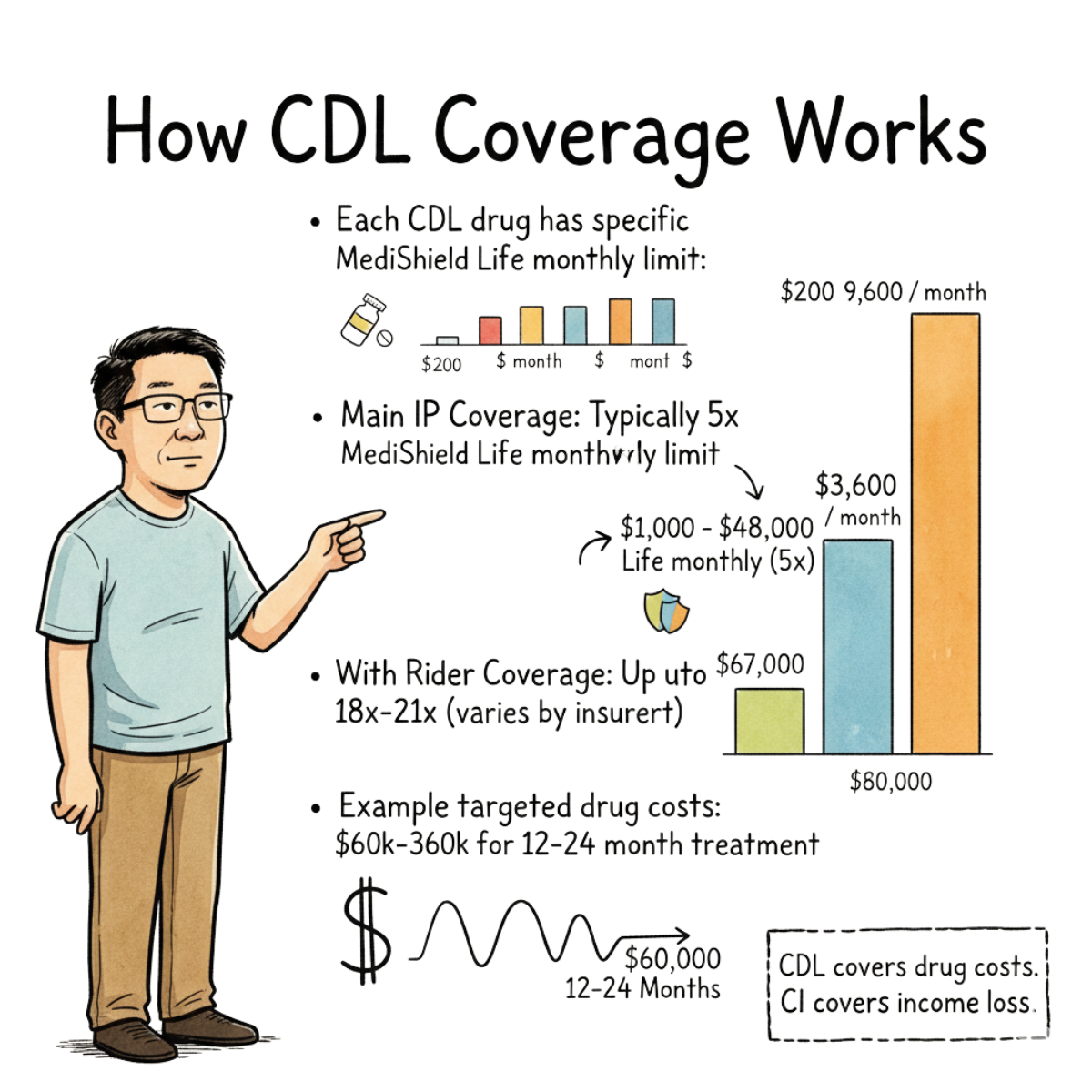

What the Cancer Drug List (CDL) Covers (And What It Doesn’t)

Singapore’s Ministry of Health maintains a Cancer Drug List for outpatient cancer drug treatments claimable under MediShield Life, MediSave, and Integrated Shield Plans.

Key implementation dates:

- September 1, 2022: CDL took effect for MediShield Life and MediSave

- April 1, 2023: CDL took effect for Integrated Shield Plans (upon renewal or new purchase)

What This Means:

Public hospitals (SGH, National Cancer Centre Singapore) dispense cancer drugs on the CDL at subsidized rates.

Your Integrated Shield Plan provides coverage as a multiple of the MediShield Life monthly claim limit for each specific CDL treatment:

- Main IP plans typically cover 5x the MediShield Life monthly limit

- With riders, coverage can increase to 18x-21x the monthly limit (varies by insurer)

Important: Each cancer drug treatment on the CDL has its own MediShield Life monthly claim limit, ranging from $200 to $9,600 per month depending on the treatment.

Example:

- Cancer Drug X has a MediShield Life limit of $2,000/month

- Your IP offers 5x coverage: You’re covered for up to $10,000/month for Drug X

- With a rider offering 18x: Coverage increases to $36,000/month for Drug X

What about treatment costs?

Some targeted cancer drugs cost $5,000-15,000 per month. If treatment lasts 12-24 months, total drug costs can reach $60,000-360,000.

With typical IP coverage of 5x MediShield Life limits, most CDL treatments are well-covered. Riders provide additional coverage for higher-cost treatments and selected non-CDL drugs.

The point: CDL coverage handles drug costs. But it doesn’t handle the income loss during the 12-24 months of treatment.

Why Critical Illness Coverage Matters More Than You Think

Hospital plans pay for treatment. MediShield Life and Integrated Shield Plans cover bills.

But what pays for the 6-12 months when you can’t work full-time?

Critical illness coverage pays a lump sum on diagnosis. Typically $50,000 to $200,000+ depending on your policy.

Industry recommendation: The Life Insurance Association (LIA) Singapore recommends obtaining critical illness protection equivalent to 4 times your annual income to provide essential financial support for household expenses during the recovery period.

This lump sum replaces income when:

- You’re taking unpaid leave for treatment

- You’re working reduced hours during recovery

- You’re the caregiver taking time off to support a family member

- You need to hire help for childcare, eldercare, or household management

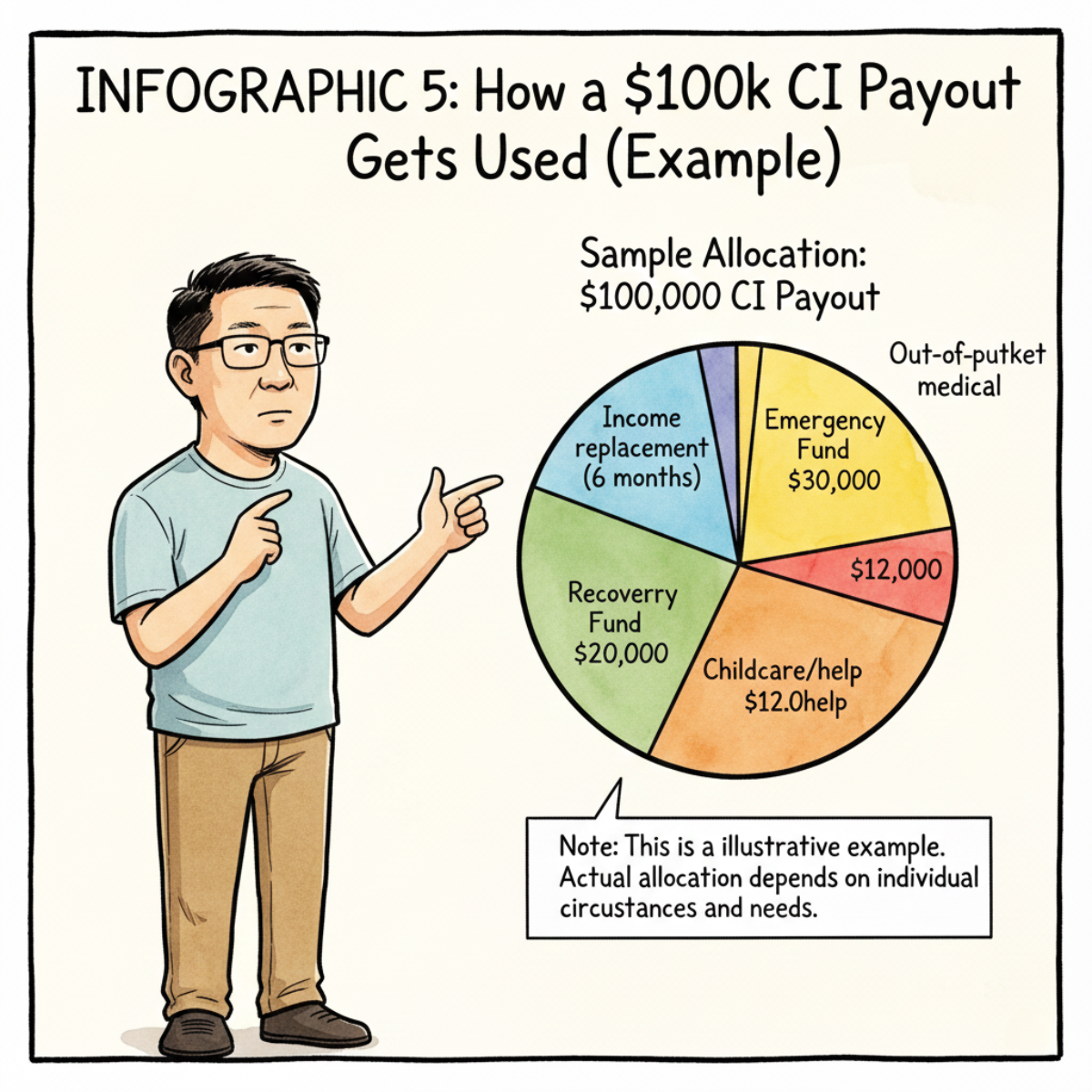

Example scenario:

You’re diagnosed with stage 1 cancer. Your CI policy pays out $100,000.

You use it to:

- Replace 6 months of lost income ($30,000)

- Cover out-of-pocket medical costs not covered by insurance ($10,000)

- Hire part-time help for childcare during treatment months ($12,000)

- Build a buffer for recovery phase when you’re back to work but not full capacity ($20,000)

- Keep the rest as emergency fund ($28,000)

Without CI coverage:

- You’re burning through savings or taking on debt

- Financial stress compounds medical stress

- You might return to work too early because you can’t afford not to

Planning for Time, Not Just Money

Most people plan for hospital bills. Few people plan for the months of disrupted life that come with treatment.

Here’s a simple framework:

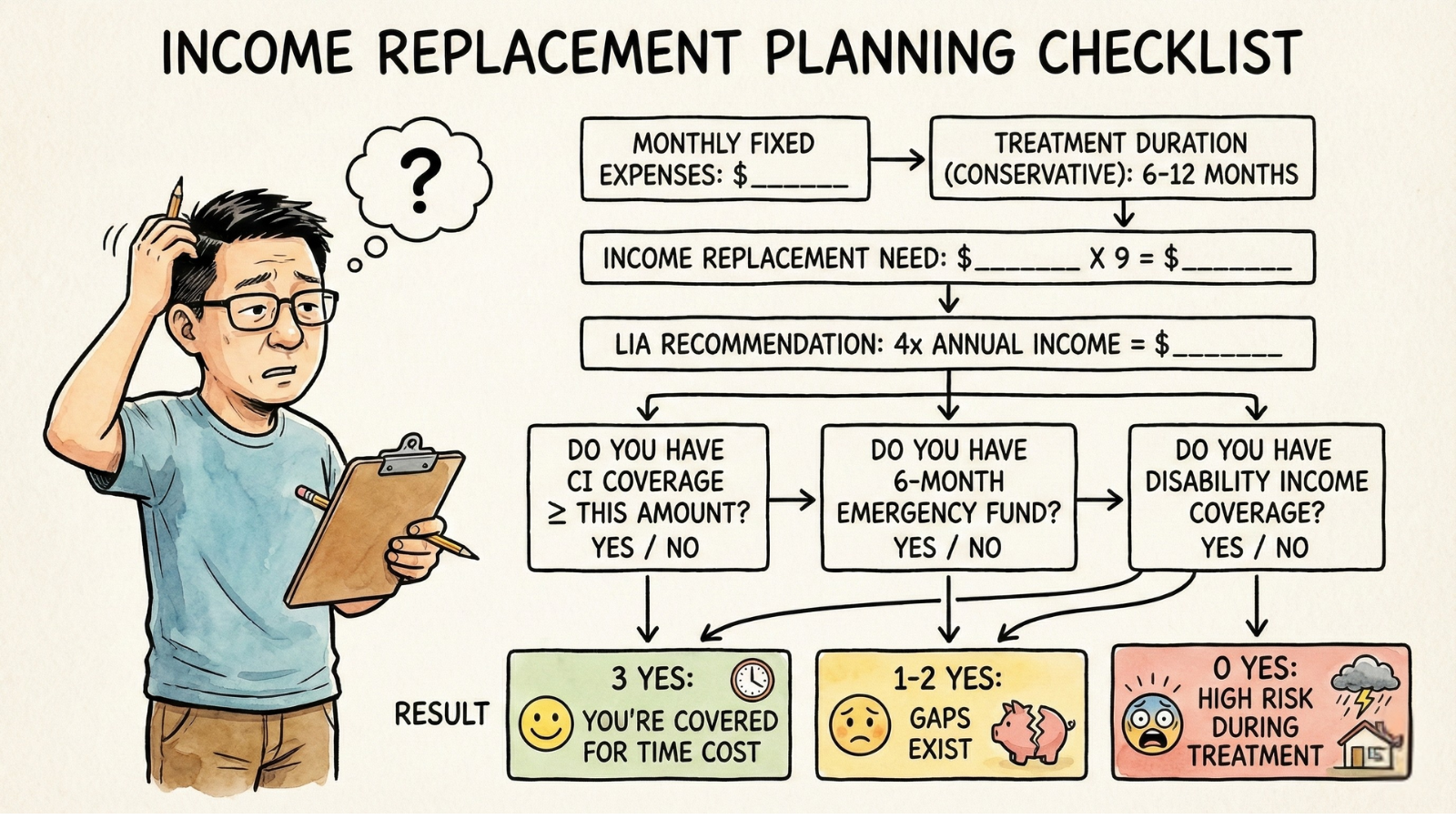

Step 1: Calculate Your Monthly Fixed Commitments

List everything that doesn’t stop when treatment starts:

- Mortgage/rent

- Utilities

- Insurance premiums

- School fees

- Parent support

- Debt payments

Total monthly fixed: $________

Step 2: Estimate Treatment Duration

Conservative planning assumptions:

- Early-stage cancer: 6-12 months active treatment + recovery

- Injury requiring surgery: 3-6 months disrupted capacity

- Chronic illness flare-up: 3-9 months reduced work capacity

Step 3: Calculate Income Replacement Need

Monthly fixed commitments × Treatment months = Income replacement target

Example: $5,000/month × 9 months = $45,000

Add: Out-of-pocket medical costs, caregiver expenses, recovery buffer

Industry standard: LIA Singapore recommends 4x annual income for CI coverage

Step 4: Check Your Coverage

Do you have:

- CI coverage that pays at least 9-12 months of fixed expenses (or 4x annual income)?

- Disability income that replaces 50-70% of salary if you can’t work?

- Adequate emergency fund (6 months minimum)?

If no: There’s a gap. Treatment might be covered, but financial survival during treatment isn’t.

What I Wish I’d Known Before My Mom’s Diagnosis

Looking back, here’s what would’ve helped:

1. Build a bigger emergency fund than you think you need

We thought 3 months was enough. Treatment lasted 9 months (including recovery). We should’ve had 12 months liquid.

2. Check CI coverage before you need it

My mom had CI coverage, but it was set up when she was 30. The payout didn’t match her current income needs. We should’ve reviewed it every 5 years.

3. Understand your employer’s leave policy

Some employers offer extended medical leave. Some don’t. Know what’s available before you need it.

4. Plan for caregiver time

I underestimated how much time I’d need to take off. If you’re the primary caregiver, factor in substantial time commitments during active treatment.

5. Don’t assume “early stage” means “quick recovery”

Early stage is good news. But it still means months of treatment. Plan conservatively.

Final Thought

A diagnosis arrives without warning. Recovery takes months on the calendar.

Hospital insurance covers bills. Critical illness coverage covers time.

Most people plan for one. They forget about the other.

If this feels close to home, or if you’re not sure whether your coverage handles both bills and time, reach out. A review often reveals gaps before stress hits.

If you want to review your CI coverage and make sure it actually replaces income during treatment months, let’s talk. I’ll show you where the gaps are and what it would take to close them.