Navigating inheritance laws can be complex, especially in Southeast Asia, where cultural diversity has heavily shaped legal structures. Both Indonesia and Singapore recognize the diverse religious and cultural backgrounds of their populations by utilizing pluralistic legal systems. However, their underlying approaches to property, wills, and familial obligations differ significantly due to their distinct historical roots—Indonesia’s foundation in Dutch Civil Law versus Singapore’s basis in English Common Law.

Here is a look at how these two neighboring nations handle the distribution of an estate.

1. The Core Legal Frameworks: Dual vs. Pluralistic Systems

Both nations separate inheritance laws primarily based on religion, specifically distinguishing between Muslims and non-Muslims.

-

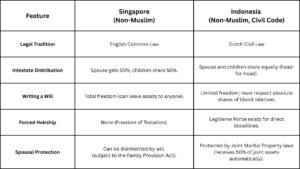

Singapore (Dual System): Singapore operates a relatively streamlined dual system. Inheritance for Muslims is governed by the Administration of Muslim Law Act (AMLA) and administered by the Syariah Court. For non-Muslims, the system is governed by civil statutes—primarily the Wills Act and the Intestate Succession Act—handled in the civil courts.

-

Indonesia (Pluralistic System): Indonesia’s legal landscape is more intricate. Inheritance can fall under three different jurisdictions depending on the deceased’s background and choices:

-

Islamic Law (Kompilasi Hukum Islam / KHI): Applies to Muslims, administered by the Religious Courts.

-

Civil Code (KUHPerdata / Burgerlijk Wetboek): Applies primarily to non-Muslims and citizens of European or Chinese descent, administered by District Courts.

-

Customary Law (Hukum Adat): Unwritten, community-specific laws that vary across Indonesia’s diverse ethnic groups, prioritizing communal harmony and familial lineage.

-

2. Intestate Succession: Dying Without a Will

When someone dies without leaving a will (ab intestato), both countries have statutory formulas to distribute the assets, but the hierarchies differ.

In Singapore (Non-Muslim):

Under the Intestate Succession Act, the distribution is quite rigid and prioritizes the spouse and children.

-

Spouse and Children: If both survive, the spouse receives 50%, and the children equally share the remaining 50%.

-

Spouse only (no children, no parents): The spouse receives 100%.

-

No Spouse or Children: The estate moves up to parents, then siblings, then grandparents, and finally uncles/aunts.

In Indonesia (Non-Muslim under Civil Code):

Under the KUHPerdata, heirs are divided into four strict groups (Golongan). Group I completely excludes Group II, and so on.

-

Group I (Spouse and Children): The surviving spouse and all legitimate children share the inheritance estate equally, head-for-head. (e.g., A wife and two children would each get 1/3 of the deceased’s estate).

-

Note on Marital Assets: In Indonesia, before inheritance is calculated, the surviving spouse automatically retains 50% of all joint marital assets acquired during the marriage. Only the deceased’s half, plus any personal pre-marital assets, falls into the inheritance pool.

3. The Great Divide: Testamentary Freedom vs. Forced Heirship

The most stark contrast between Singaporean and Indonesian inheritance law for non-Muslims lies in how much control a person has over their own assets when writing a will.

Singapore: Freedom of Testation (Common Law)

Because Singapore follows English Common Law, non-Muslims enjoy total testamentary freedom. You can write a will leaving 100% of your assets to a friend, a charity, or a single child, completely disinheriting your spouse or other family members if you wish.

-

The Caveat: The only safety net is the Inheritance (Family Provision) Act. If a deceased fails to make “reasonable provision” for a dependent (like a spouse, infant, or disabled child), the dependent can apply to the court for financial maintenance from the estate.

Indonesia: Forced Heirship / Legitieme Portie (Civil Law)

Rooted in Dutch Civil law, Indonesia’s KUHPerdata strictly limits testamentary freedom through a concept called Legitieme Portie (LP), or the absolute statutory share.

-

The law mandates that direct bloodline relatives (children, grandchildren, or parents if there are no descendants) are guaranteed a specific percentage of the estate that cannot be overridden by a will.

-

For example, if a man tries to leave all his money to charity, his legitimate children can legally contest the will to claim their Legitieme Portie. Interestingly, a spouse is tied by marriage, not blood, and therefore has no Legitieme Portie under Indonesian Civil Code (though they are still protected by their right to 50% of the joint marital assets).

Conclusion

While both Singapore and Indonesia accommodate their diverse populations through separate legal frameworks for Muslims and non-Muslims, their secular laws diverge greatly. Singapore prioritizes the individual’s right to distribute their wealth as they see fit, reflecting its Common Law heritage. In contrast, Indonesia’s Civil Code prioritizes the preservation of bloodlines, legally forcing individuals to leave a portion of their wealth to direct descendants regardless of their personal wishes.

Navigating cross-border estate planning and complex inheritance laws requires specialized guidance. Ensure your assets are protected and your family’s future is secure with expert advice. Book your Financial Advisory Consultation with us now.