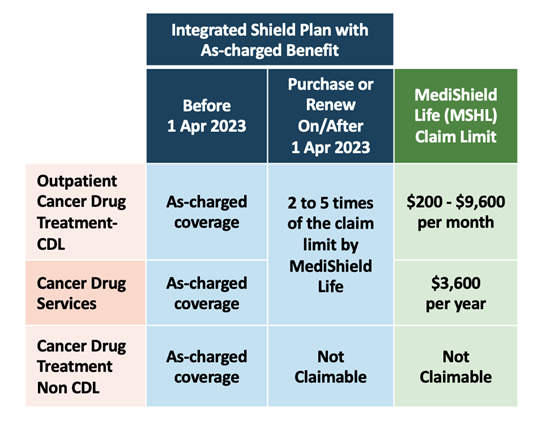

In addition to specifying the drug and type of cancer, the CDL also introduces limits on MediShield Life claims and the maximum amount of MediSave allowed to be used. In the past, the majority of Integrated Shield Plans operate on an as-charged basis.

Under this round of changes, separate claim limits for cancer drug services have been introduced. These cover ancillary procedures that are part of the cancer treatment, including consultations, scans, lab investigations, chemotherapy preparations, supportive care drugs and blood transfusions.

This means that if a particular approved treatment on the CDL costs more than the allowable MediShield Life claim limit, patients would need to claim against their integrated shield plans – up to the policy limits. If this is still insufficient, patients will then need to top-up any shortfall in cash.

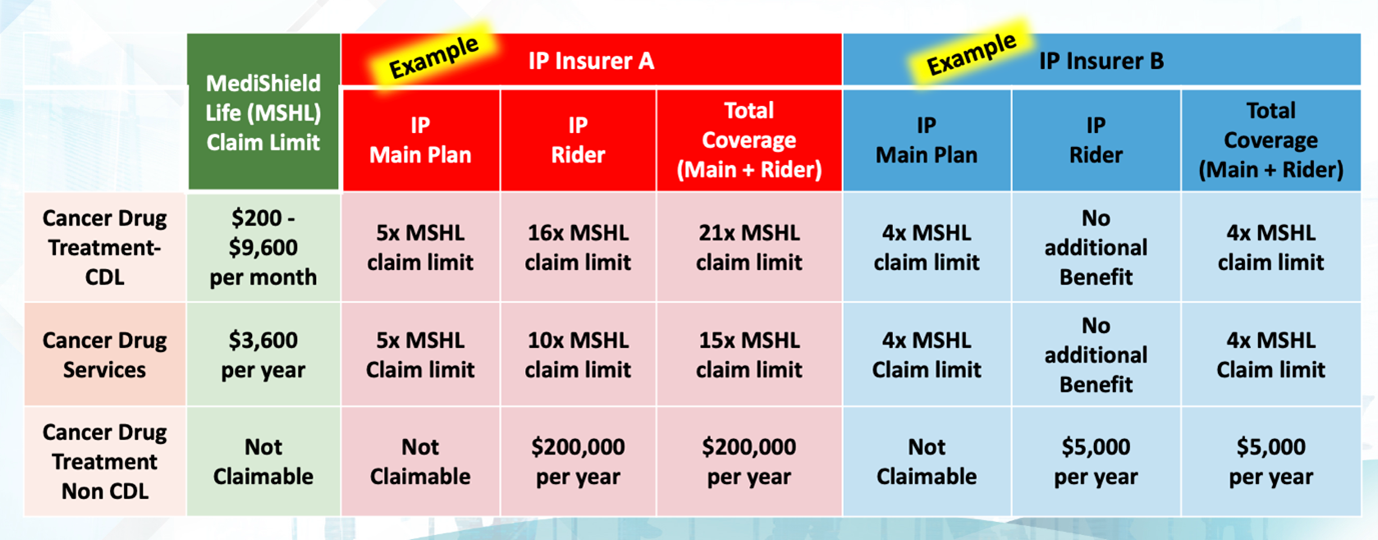

In response to the Cancer Drug List (CDL), Integrated Shield Plan (IP) providers have started to offer rider plans for IP policyholders to enhance outpatient cancer drug treatment coverage.

However, it is important to realise that IP riders’ coverage differs significantly among the IP insurers. Therefore, the impact on IP policyholders varies depending on the IP rider’s coverage level.