You can’t plan 2026 if you don’t understand what happened in 2025.

Every December, people start thinking about New Year’s resolutions. Lose 10kg. Save $20,000. Get promoted. Start a side business.

By February, most of those resolutions are forgotten.

The problem isn’t the goals. It’s the starting point.

Most people set January goals without reviewing December reality. They don’t know what worked this year. They don’t know what failed. They don’t know where they got lucky versus where they were prepared.

So they plan blind. And blind plans rarely survive contact with reality.

What December Is Actually For

December isn’t just the end of the year. It’s the review period before the planning period.

If you skip the review, your 2026 plan is built on assumptions, not data. You’ll repeat the same mistakes. You’ll miss the same gaps. You’ll set goals that don’t address the actual problems.

December clarity leads to January strategy.

Here’s what you should be reviewing before you start planning 2026.

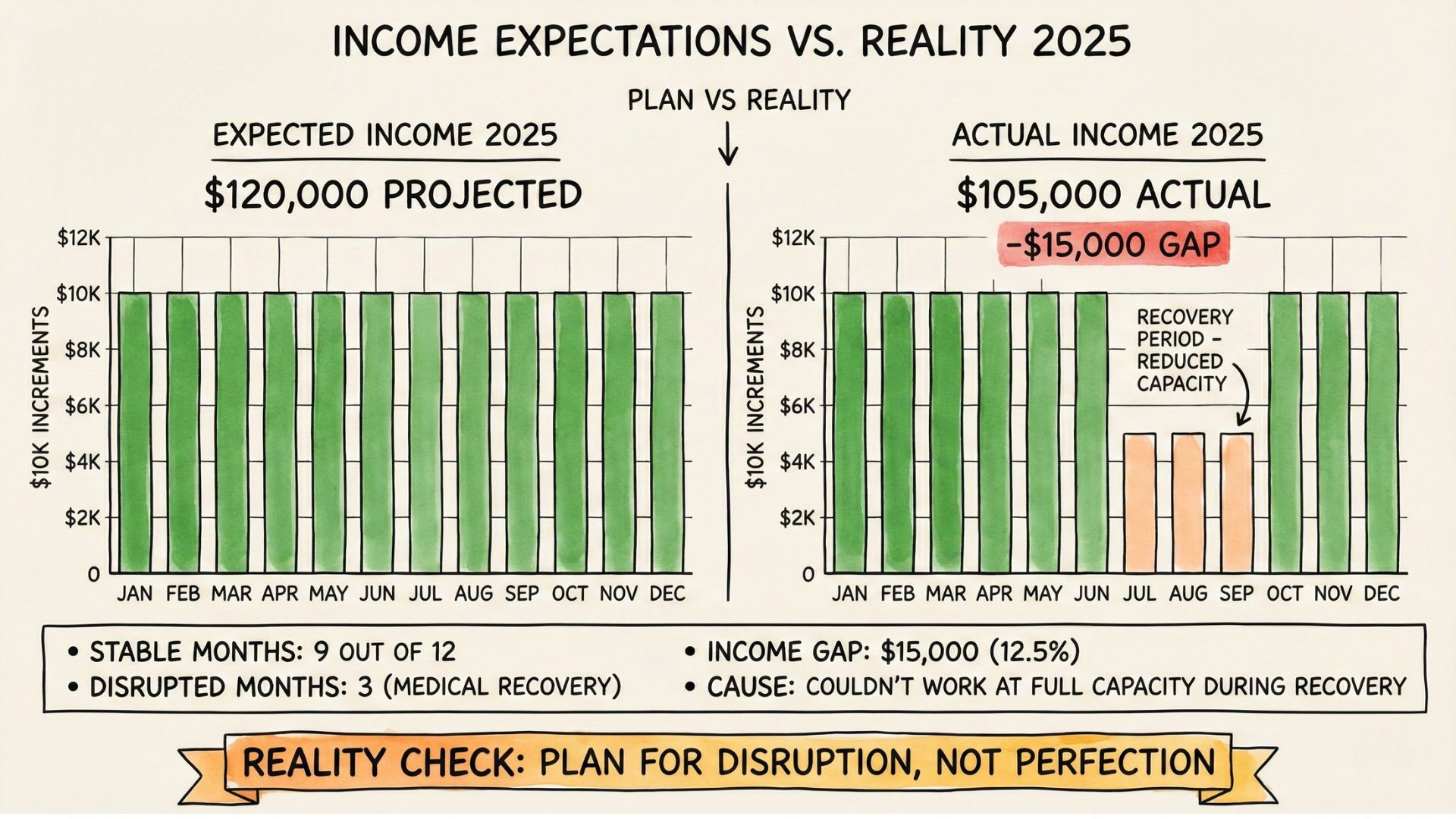

1. Income Review: What Actually Came In

Pull up your bank statements. Add up every income source for 2025.

Questions to ask:

- Did you earn more or less than you expected?

- Which income sources were stable? Which were variable?

- Did any unexpected income arrive? (Bonuses, gifts, side projects)

- Did any expected income fail to materialize?

Why this matters: Your 2026 budget depends on realistic income projections. If you assume you’ll earn what you hoped to earn (not what you actually earned), your plan is already broken.

Example from my year: I expected stable income all year. Two surgeries meant three months of reduced capacity. My income dropped during recovery. That wasn’t in the plan. Now I know: I need a bigger emergency fund to cover months when I can’t work at full capacity.

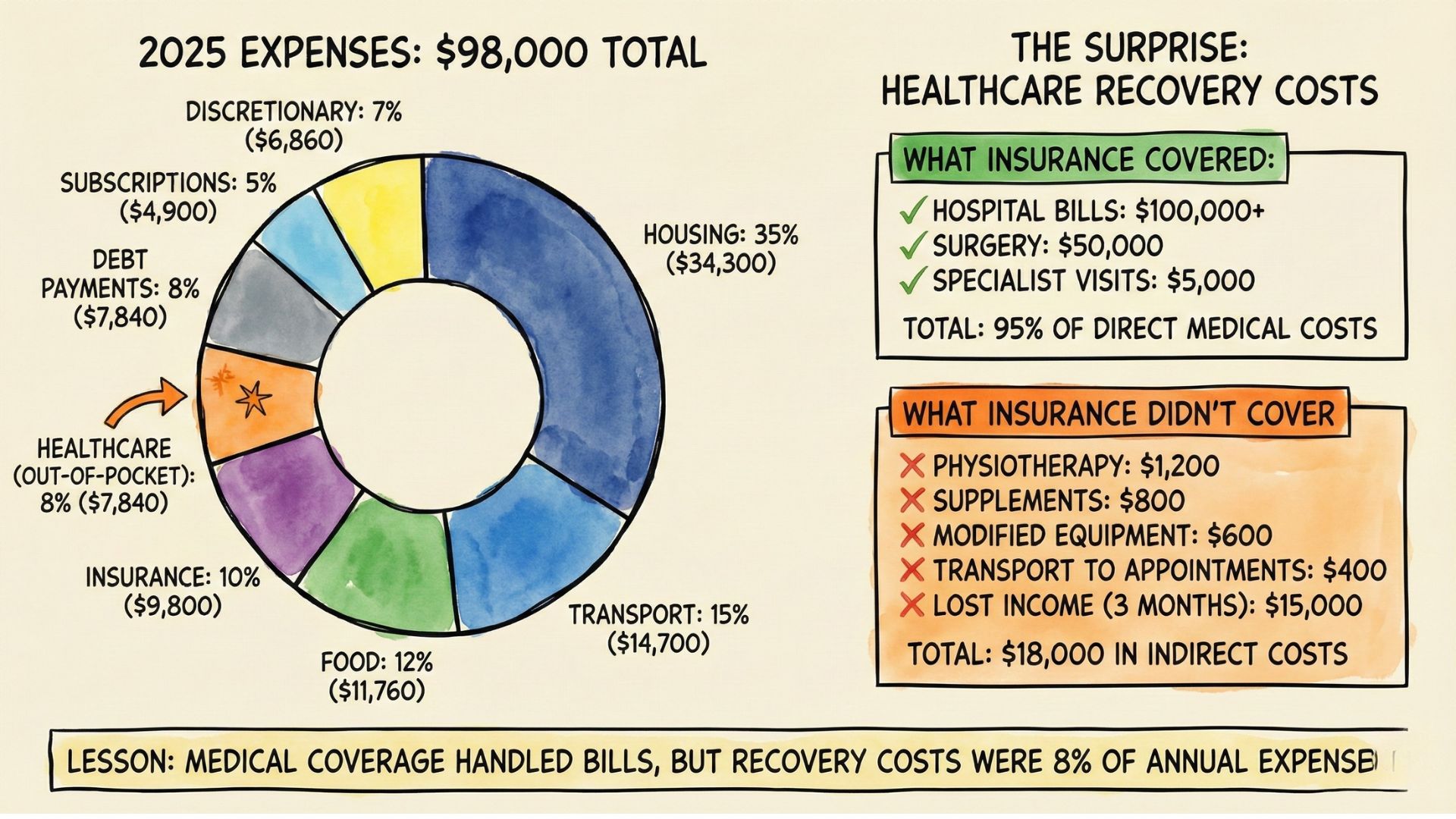

2. Expense Review: Where Money Actually Went

List your major expense categories for 2025:

- Housing (mortgage/rent, utilities, maintenance)

- Transport (car loan, petrol, public transport)

- Food (groceries, dining)

- Insurance (life, health, property)

- Healthcare (out-of-pocket medical costs)

- Debt payments (credit cards, loans)

- Subscriptions (streaming, gym, software)

- Discretionary (travel, hobbies, entertainment)

Questions to ask:

- Which expenses were fixed? Which were flexible?

- Which expenses increased unexpectedly?

- Which expenses could you cut without impacting quality of life?

- Which expenses were worth it? Which weren’t?

Why this matters: You can’t save more in 2026 if you don’t know where money went in 2025. Vague goals (“spend less on dining”) fail. Specific insights (“we spent $600/month on food delivery because we were too tired to cook after work”) lead to actual solutions.

Example from my year: Hospital costs were covered by insurance. But recovery costs weren’t. Physiotherapy, supplements, modified training equipment—those added up to $3,000 over three months. None of that was in my budget. Now I know: medical coverage isn’t just about hospital bills.

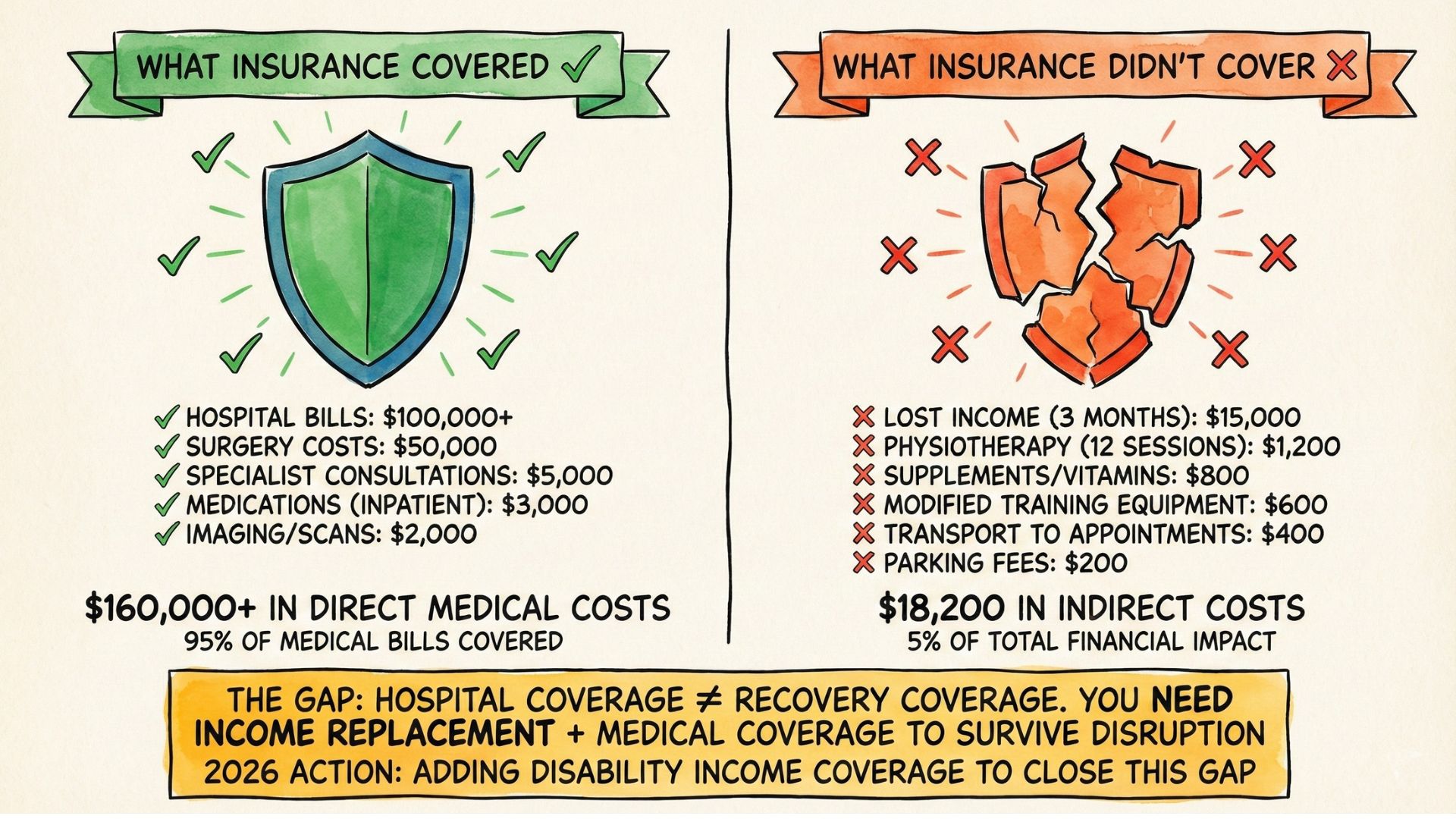

3. Coverage Gaps: What Insurance Didn’t Cover

If you had any medical events, claims, or close calls this year, review what was covered and what wasn’t.

Questions to ask:

- Did you make any insurance claims? Were they fully covered?

- Were there out-of-pocket costs you didn’t expect?

- If you couldn’t work for 6 months, would you have been financially okay?

- If a family member got sick, could you afford time off to care for them?

Why this matters: Coverage gaps only show up under stress. If 2025 was smooth, that’s great. But if something went wrong, the gaps are now visible. Don’t ignore them.

Example from my year: My hospital coverage worked perfectly. My rider covered the deductible. But I didn’t have disability income insurance. If I’d been unable to work for six months (not just reduced capacity, but completely unable), I would’ve burned through savings. That’s a gap I’m fixing in 2026.

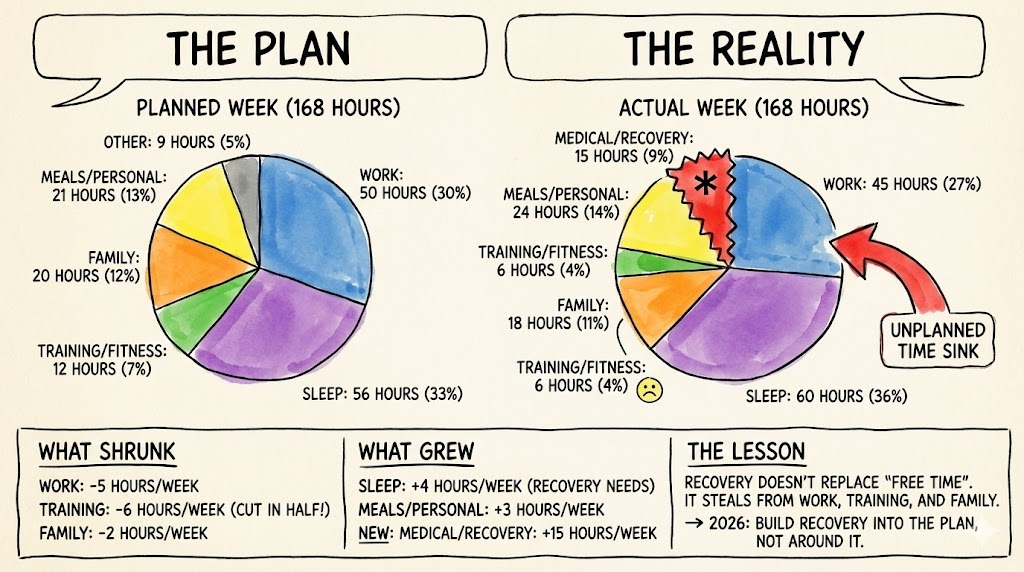

4. Time Allocation: Where Hours Actually Went

Money isn’t the only resource. Time matters too.

Questions to ask:

- How many hours per week did you actually work? (Not “supposed to”—actually did)

- How much time did you spend on family, fitness, hobbies, rest?

- Which time investments paid off? Which didn’t?

- Where did time disappear without you noticing?

Why this matters: If you plan to “work out 5x per week” in 2026 but you barely managed 2x per week in 2025, your plan isn’t realistic. Either you need to restructure your time, or you need to set different goals.

Example from my year: I planned to train 6 days per week. Injuries meant I trained maybe 3 days per week for half the year. My 2026 goal isn’t “train more.” It’s “structure training to account for recovery time and avoid overtraining injuries.”

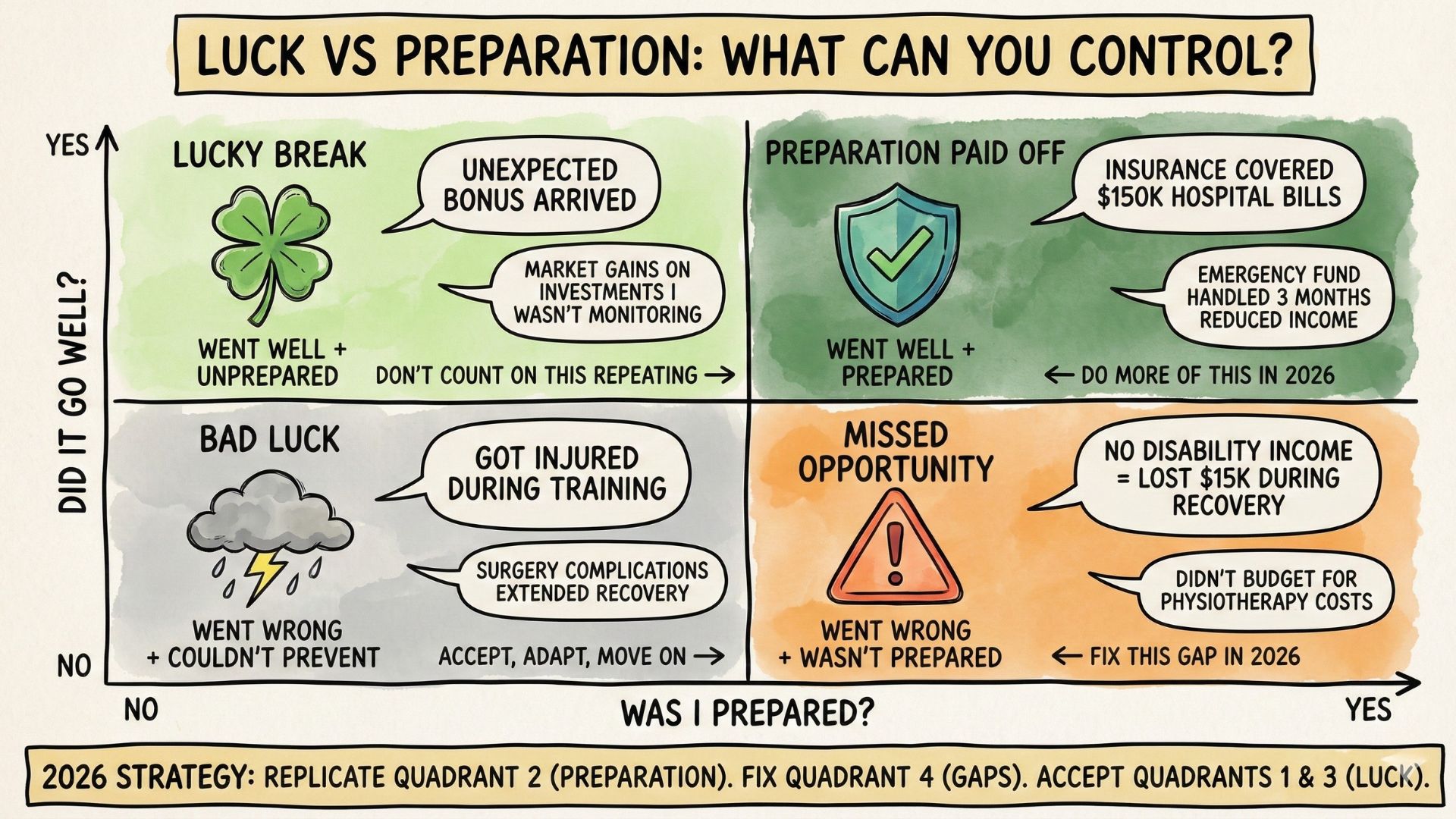

5. Luck vs Preparation: What You Can Control

Some things went right this year because you were lucky. Some things went right because you were prepared. Knowing the difference matters.

Questions to ask:

- What went well that you didn’t plan for? (Luck)

- What went well because you prepared in advance? (Preparation)

- What went wrong that you could’ve prevented? (Lack of preparation)

- What went wrong that was out of your control? (Bad luck)

Why this matters: You can’t count on luck in 2026. But you can count on preparation. If something good happened by accident, don’t assume it’ll happen again. If something good happened because you planned for it, do more of that.

Example from my year: My hospital stays didn’t bankrupt me because I had coverage. That wasn’t luck. That was preparation from years ago when I set up my insurance properly. But my recovery was faster than expected because I’d maintained fitness before the injury. That was half preparation (I trained consistently), half luck (my body healed well).

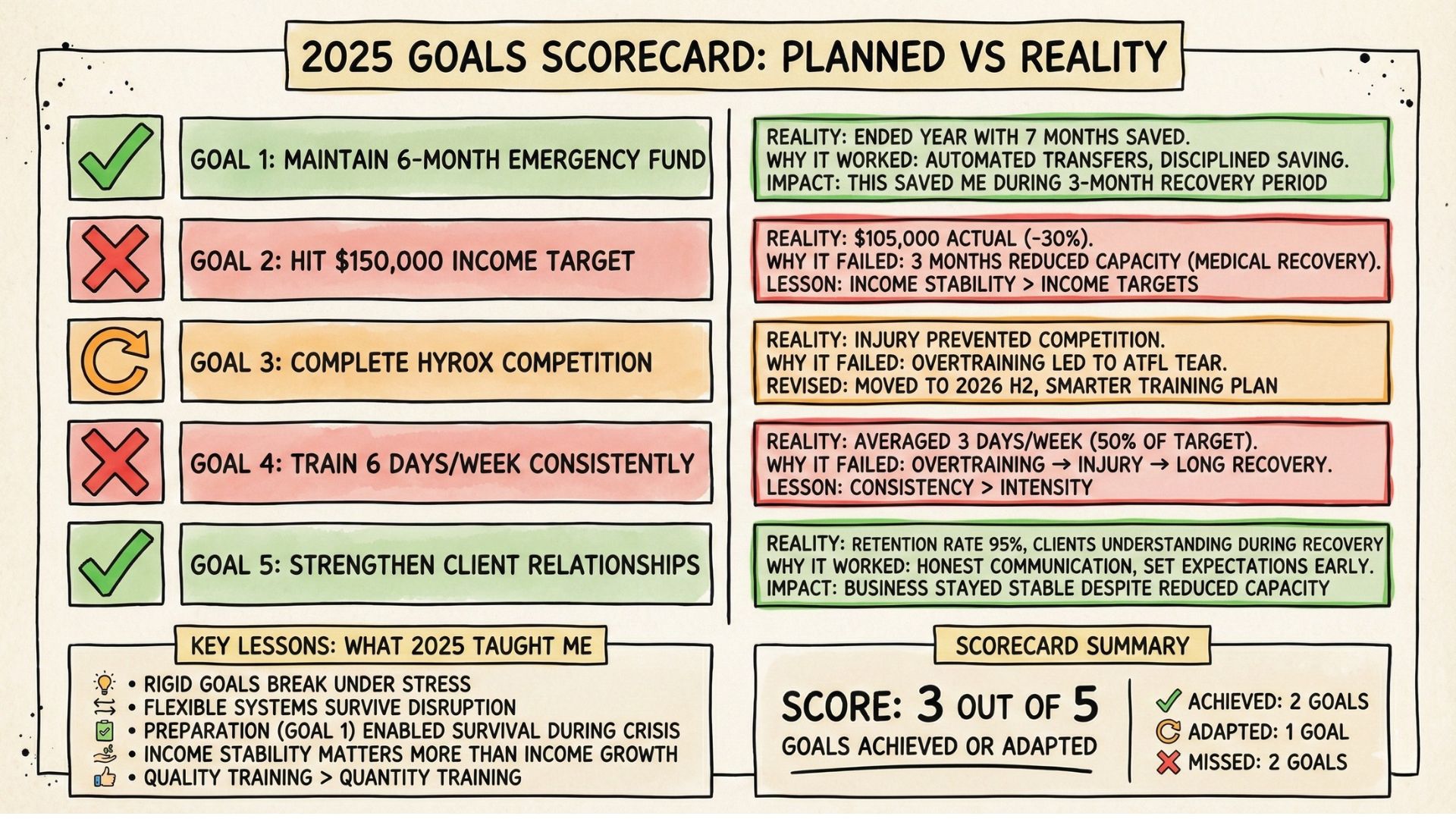

6. Goals vs Reality: What You Actually Achieved

Pull up your 2025 goals. Be honest: how many did you hit?

Questions to ask:

- Which goals did you achieve?

- Which goals did you miss? Why?

- Were the goals realistic to begin with?

- Did your priorities change midyear?

Why this matters: If you missed most of your 2025 goals, either the goals were wrong or your approach was wrong. Don’t just copy-paste the same goals into 2026. Understand why they didn’t happen.

Example from my year: I wanted to hit specific income targets. I missed them because I couldn’t work at full capacity for three months. But I also realized the income target was arbitrary. What I actually needed was income stability and liquidity during disruptions. That’s a different goal.

7. Relationships: Who Showed Up

2025 tested relationships. Who showed up when things got hard?

Questions to ask:

- Who supported you this year?

- Who did you support?

- Which relationships added value to your life?

- Which relationships drained energy without giving back?

Why this matters: Your 2026 plan should include time for people who matter. It should also include boundaries around people who don’t.

Example from my year: My wife showed up every single time. My clients were understanding when I needed to reschedule. My team carried work I couldn’t handle. Those relationships matter. I’m structuring 2026 to protect time with them.

What to Do With This Information

Once you’ve reviewed 2025, you have data. Now use it.

Step 1: Identify patterns

- What kept going wrong? (Recurring problem = structural issue)

- What kept going right? (Recurring success = do more of this)

Step 2: Spot the gaps

- Where were you exposed to risk?

- Where did you lack preparation?

- Where did you rely on luck?

Step 3: Set 2026 priorities

- Fix the gaps first (emergency fund, insurance coverage, time structure)

- Double down on what worked (relationships, habits, systems)

- Drop what didn’t (goals that don’t align with reality, time sinks, energy drains)

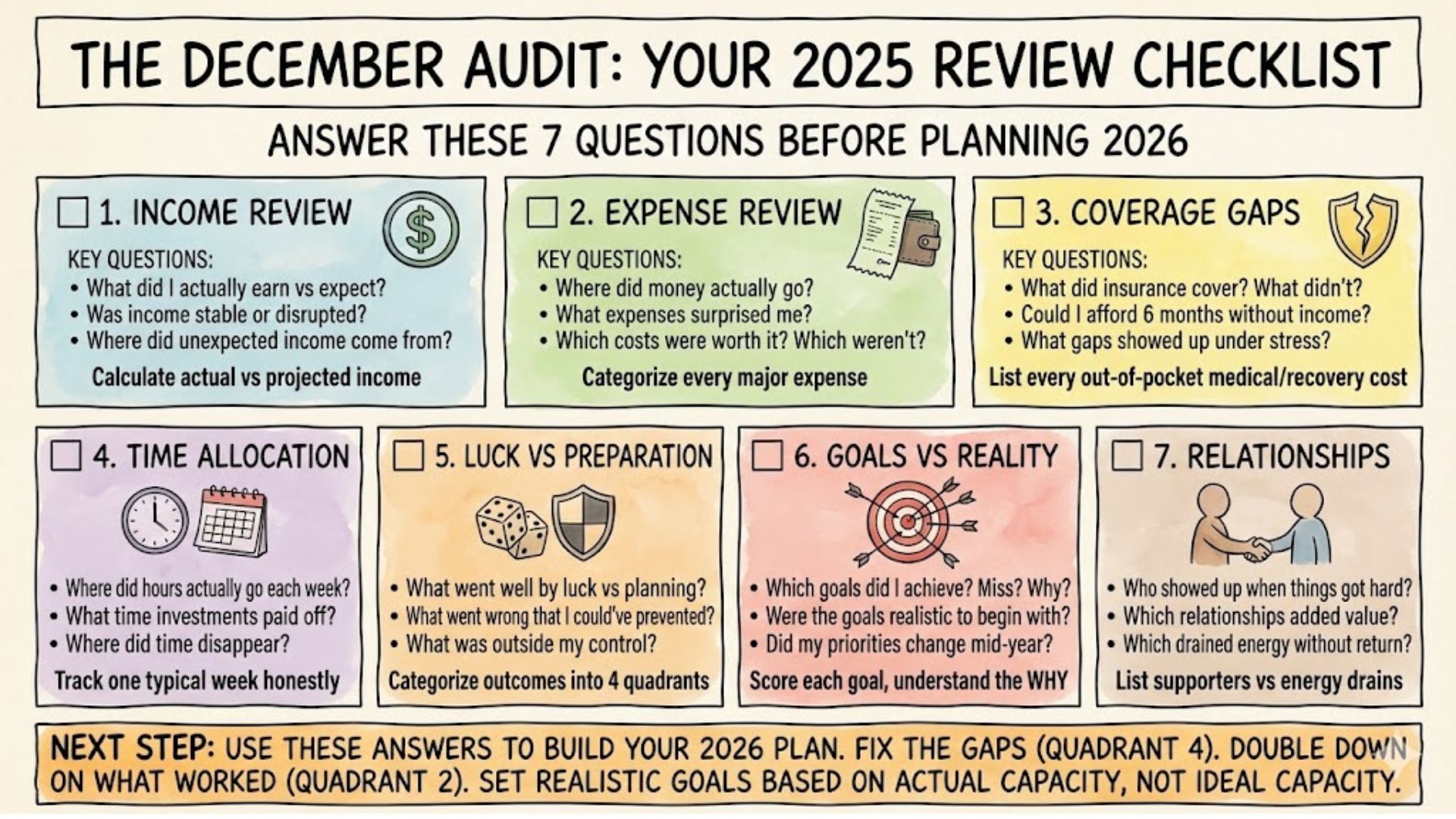

The December Audit Checklist

Before you plan 2026, answer these:

- Income: What did I actually earn? Was it stable?

- Expenses: Where did money go? What surprised me?

- Coverage: What insurance gaps showed up this year?

- Time: Where did hours actually go? What paid off?

- Luck vs Prep: What can I control going forward?

- Goals vs Reality: What did I achieve? What did I miss? Why?

- Relationships: Who showed up? Who drained energy?

If you can answer these, your 2026 plan will be based on reality, not hope.

Final Thought

January is when people make plans. December is when reality shows up.

Don’t skip the review. The gaps matter more than the goals.

If you’re not sure where to start, review your bank statements, your insurance coverage, and your calendar. Those three sources will tell you most of what you need to know.

If you want help reviewing your financial coverage and making sure 2026 doesn’t have the same gaps as 2025, reach out. A year-end review often reveals things you didn’t know were missing.