The Speed Gap: Public vs Private Hospital Wait Times

Here’s the reality of hospital wait times in Singapore.

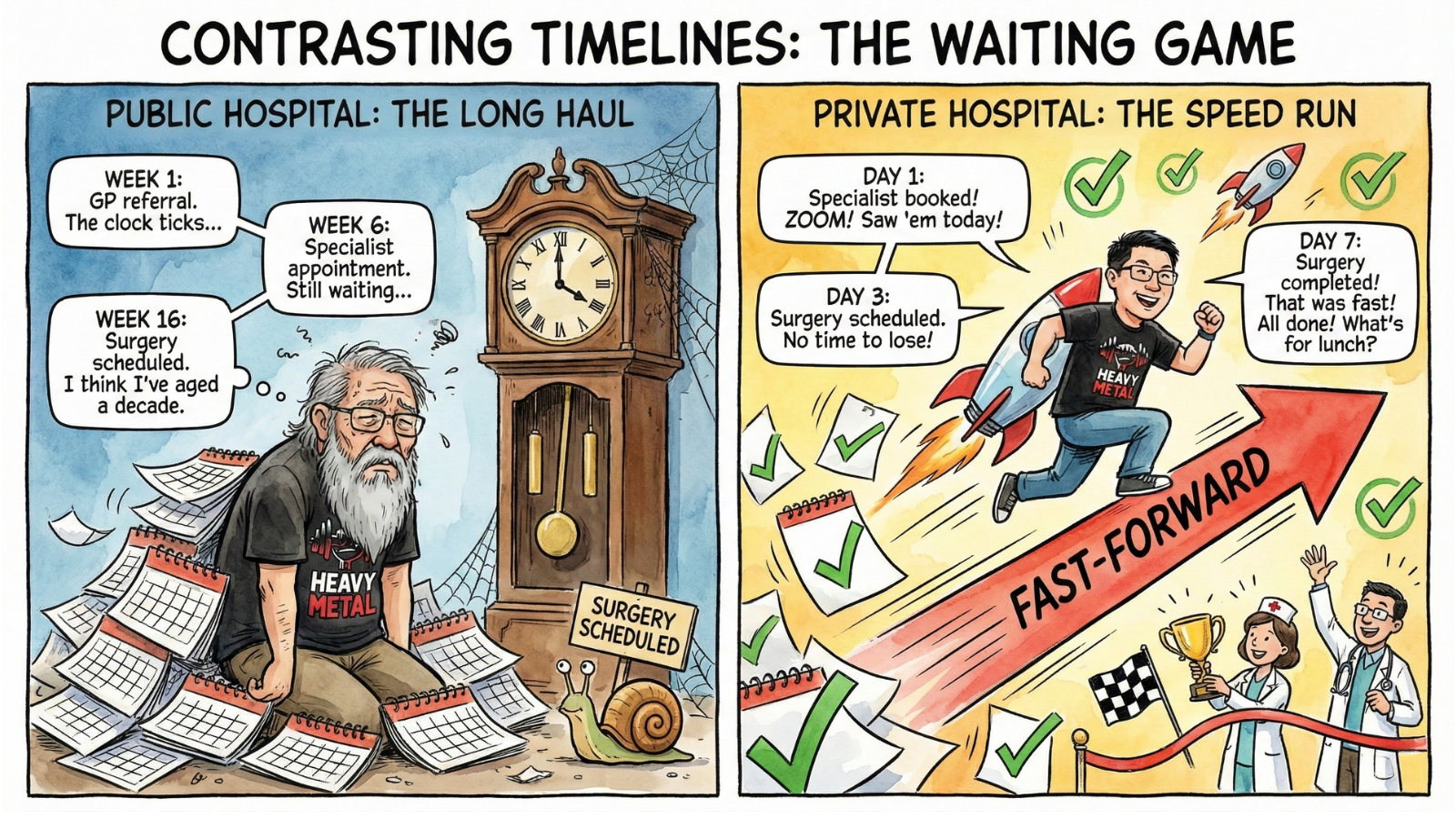

Public hospitals like SGH, TTSH, and NUH operate on a triage system. Emergency cases get prioritized. Non-urgent surgeries queue. If your condition isn’t critical, you wait.

For non-urgent surgery, the typical wait time is two to four months. Specialist appointments take four to eight weeks just for the first consultation. Then you wait again for surgery dates, imaging, follow-ups.

Private hospitals like Mount Elizabeth, Gleneagles, and Raffles work differently. Non-urgent surgery can happen within one to two weeks, sometimes the same week if schedules align. Specialist appointments happen within days, sometimes same-day. Scheduling is flexible. Queues are shorter.

The difference isn’t clinical skill. It’s system capacity and patient volume.

I tore my ATFL in July. If I’d gone through the public system, I’d have waited until September or October for surgery. Instead, I was in the operating theatre within a week.

That’s not because I chose the “best” hospital. It’s because my insurance plan gave me private hospital access.

Speed matters when you can’t work properly while injured. When pain affects daily function. When delay worsens the condition. When three months of waiting means three months of lost income, missed training,

disrupted life.

The question isn’t just “can I afford private healthcare?” It’s “can I afford to wait?”

What Your Plan Actually Covers (And What Determines Speed)

Most people think hospital insurance is simple. You get sick, insurance pays the bill. But what determines speed isn’t the hospital you choose. It’s your plan type.

Here’s the breakdown.

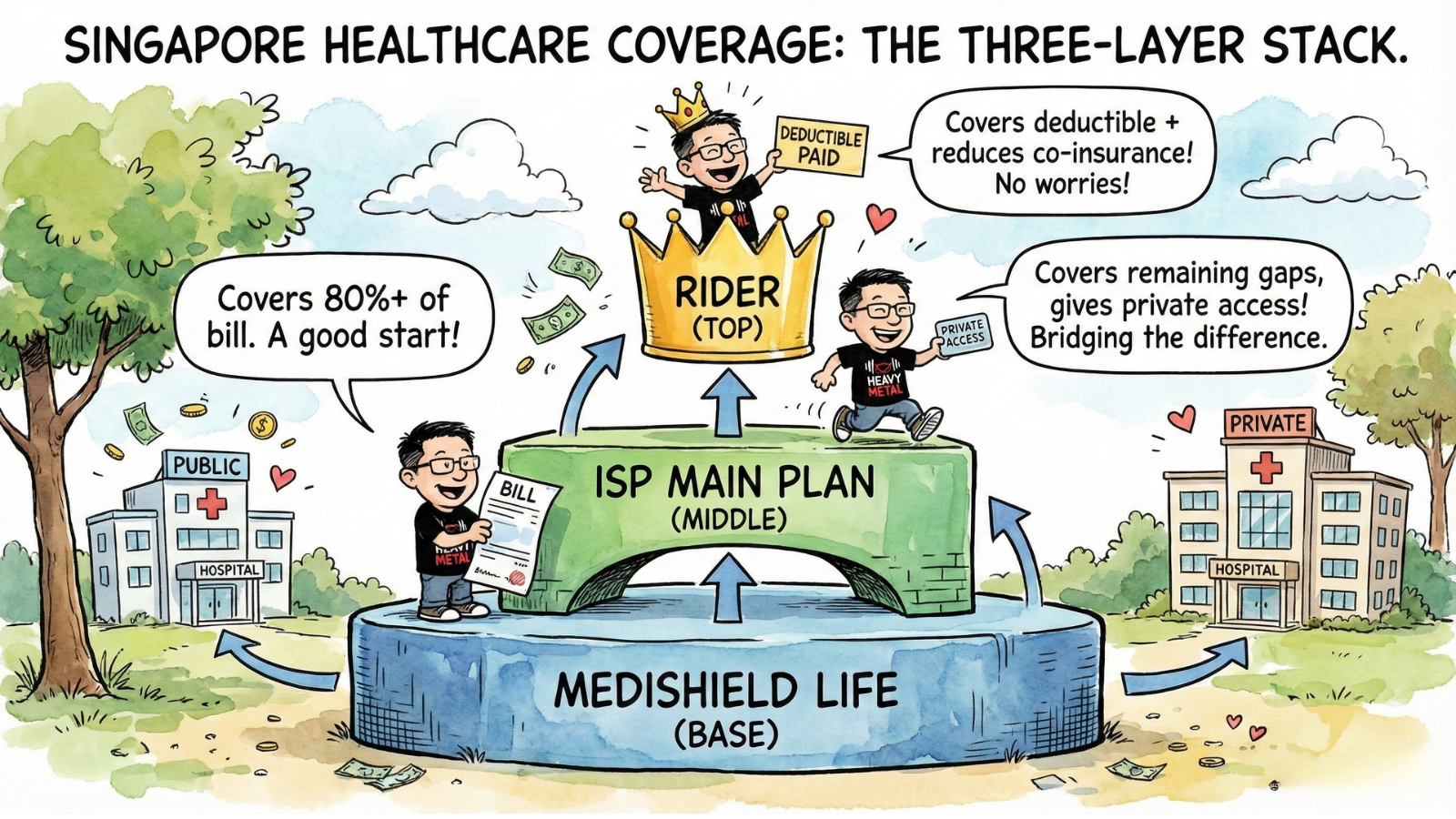

MediShield Life is the basic government plan. Every Singaporean and Permanent Resident has it. It covers public hospital stays in B2 or C class wards. It does not cover private hospitals. It does not give you faster access. It’s mandatory, but limited in scope.

If you only have MediShield Life, you’re waiting in the public system queue. Speed isn’t an option for non-urgent cases.

Integrated Shield Plans are the upgrade. These are private plans offered by insurers like HSBC, Income, AIA, Prudential, and others. The main plan covers private hospital stays. This is what gives you speed and access.

When you have an ISP main plan, you can book private hospitals. You can see specialists within days. You can schedule surgery within weeks instead of months.

The catch? There’s a deductible. Typically $3,500 for private hospitals. And there’s co-insurance, typically 10% of the bill after the deductible. So if your surgery costs $100,000, you pay $3,500 plus 10% of the remaining $96,500. That’s about $13,000 out of pocket.

Riders are optional add-ons to ISPs. They cover the deductible. They reduce co-insurance from 10% down to 5%. They make private hospital care cheaper for you.

But here’s what surprised me: the rider doesn’t give you speed. The main plan does.

I thought my rider was the reason I could access private hospitals quickly. It’s not. The main plan gave me access. The rider just reduced my out-of-pocket costs.

This matters because if you’re paying $4,000 to $9,000 per year for a rider (common for people over 50), you’re not paying for speed. You already have speed through your main plan. You’re paying to reduce your deductible and co-insurance.

My hospital claims this year totaled around $150,000. Here’s how it broke down.

MediShield Life covered about $80,000. That’s the majority of the bill. The main plan covered about $55,000. The rider covered about $15,000, which was the deductible plus the 5% co-insurance.

The rider didn’t give me speed. The main plan did.

If you’re trying to figure out whether you have access to fast private hospital care, check whether you have an ISP main plan. If yes, you’re covered. If no, you’re limited to public hospitals and public wait times.

When Speed Is Critical (And When It’s Not)

Not every medical situation requires speed. Some conditions can wait. Others can’t.

Speed is critical when you have an injury requiring surgery. Torn ligaments like ACL, ATFL, meniscus tears. Fractures requiring pins or plates. Herniated discs affecting mobility. Waiting three months means three months of pain, reduced function, and potential worsening of the injury.

Speed matters for early-stage cancer. Treatment timelines affect outcomes. Delays can allow progression. Faster diagnosis means faster treatment. Private hospitals offer faster scans, biopsies, and specialist consultations.

Speed matters after cardiac events. If you’ve had a heart attack or stroke, follow-up care is urgent. Faster access to cardiologists and rehab programs can make a real difference. Public system queues can delay recovery protocols.

Speed matters when the condition affects your ability to work. If you can’t work while waiting for treatment, the cost isn’t just medical. It’s lost income. Three months of reduced capacity can mean three months of lost earnings, especially for self-employed workers or people on commission.

Speed matters less for routine check-ups. Chronic condition management like diabetes or hypertension can be handled at public polyclinics. Preventive screenings can be done at public health centers without issue.

The key question is: “What does waiting cost me—financially, physically, emotionally?”

For me, waiting three months meant three months of limping through client meetings, skipping F45, struggling with basic movement. The financial cost of private surgery was high. The cost of waiting would have been higher.

What To Check In Your Plan Right Now

If you’re not sure whether your plan gives you speed when you need it, here’s what to check.

First, do you have an Integrated Shield Plan? If yes, you have private hospital access. If no, you’re limited to public hospitals under MediShield Life only. Check your policy documents or call your insurer to confirm.

Second, what’s your deductible? Private hospital deductibles are typically $3,500. If you don’t have a rider, you’ll pay this out of pocket. If you have a rider, it’s covered. Ask yourself: “Can I afford $3,500 to $5,000 if I need surgery tomorrow?”

Third, what’s your co-insurance? With just a main plan, you pay 10% of the bill after the deductible. With a main plan plus rider, you pay 5%. For a $100,000 bill, that’s $10,000 versus $5,000 out of pocket. Ask: “Can I afford 5% to 10% of a major hospital bill?”

Fourth, do you have outpatient cancer drug coverage? This is called the Cancer Drug List or CDL. It covers expensive outpatient cancer drugs. Main plans typically cover five to nine times your annual claim limit. Riders can increase this to 18 times. If you’re diagnosed with cancer, CDL determines whether you can afford targeted therapy drugs. Check your policy: “Does my plan include CDL? What’s the coverage limit?”

Fifth, can you access specialists quickly? Private hospitals allow direct specialist booking with short wait times. Public hospitals require a GP referral first, then you join longer queues. Your plan determines which system you access.

Action step: pull out your policy document today. If you don’t have an ISP main plan, you don’t have speed. If you do have one, you’re covered, rider or not.

The Real Cost of Speed

Private hospital access costs more. That’s the trade-off.

My surgery bill was over $100,000. If I’d gone public, it would have been a fraction of that, maybe $10,000 to $20,000 after subsidies.

But I would have waited three months. Three months of pain. Three months of lost training. Three months of limping through work.

For me, that wasn’t acceptable. The bill was high, but the cost of waiting was higher.

Not everyone can afford private care. That’s reality. But if you can afford it and you don’t realize your plan already gives you access, you’re leaving options on the table.

Speed isn’t everything. But when your body fails you, it’s the first thing that matters.