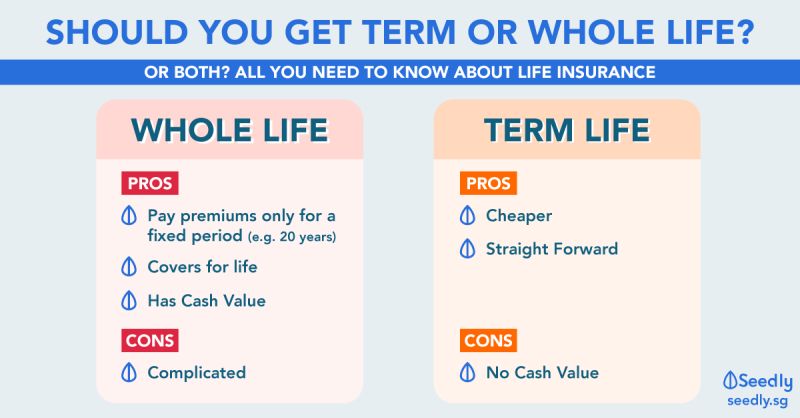

Term or Whole Life?

Choosing between term and whole life insurance has been a topic of debate for years.

To me, there is no strict right or wrong answer.

It really depends on getting a full fact find done before making any proposal. There is no cookie-cutter solution when it comes to financial planning.

I will consider the following factors, but not limited to:

1. Entry age

2. Coverage gap based on existing insurances

3. Desired period of coverage

4. TOTAL premium outlay of the two choices (not just annual)

5. Affordability based on client’s circumstances

Point number 4 is important: we do not want to be penny wise but pound foolish 🙂

Do feel free to PM me if you wish to chat more!

Important: The information and opinions in this article are for general information purposes only. They should not be relied on as professional financial advice. Readers should seek unbiased financial advice that is customised to their specific financial objectives, situations & needs. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

Published By:

Norman Ngai

I spent 16 years of my career in multinational life and general insurers in both underwriting and claim management roles. This contributed to my deep and diverse industry experience, which will benefit my individual and corporate clients.

I am a proud representative consultant of Financial Alliance now, one of the largest financial advisory firms in Singapore.

Financial Alliance partners over 50 life/general insurers, 5 investment platforms, 71 asset management companies and 5 estate planning partners.

Be assured that you are in good hands, if you wish to embark on your risk management and financial planning journey with me.

CONTACT US

- 150 Beach Road #12-01/08, Gateway West Singapore 189720

- +65 62221889

- +65 62221019

- feedback@fa.com.sg