When it comes to our health, regular check-ups, screenings, and physical assessments help us understand where we stand and what areas need attention. The same concept applies to our finances: if you are not assessing, you are guessing.

Just like physical fitness, financial fitness is about knowing where you are, setting clear goals, and having a structured plan to get there. It can make the difference between living paycheck to paycheck and building a secure, fulfilling future.

In our Financially F.I.T. program, we help clients evaluate their overall financial well-being through three pillars:

F – Financial Management,

I – Insurance Planning, and

T – Transfer of Wealth.

In this first part of the series, we’ll zoom in on Financial Management, the foundation of a healthy financial life.

1. Start with Clear Financial Goals

Every journey needs a destination. Financial goals – whether short-term or long-term, give you direction and motivation. Your time horizon matters, because it determines the kind of financial instruments you should use. For example, a 5-year goal may call for conservative investments, while a 30-year goal can afford more allocation towards growth potential.

With clear goals it’s like running for a marathon – knowing the finish line allows you to pace and prepare properly.

2. Budgeting

Start by mapping your income sources and break down your expenses into categories:

- Income: salary, bonuses, commission, rental income, dividends

- Household expenses: mortgage, bills, groceries

- Children expenses: school fees, enrichment, allowance

- Personal expenses: meals, income tax, insurance premiums, parents’ allowance, hobbies, entertainment, vacation

- Transport expenses: public transport, petrol, vehicle loan

Knowing where your money comes and goes helps you portion it into a budgeting guide, with neat compartments: essentials, wants, savings and investing.

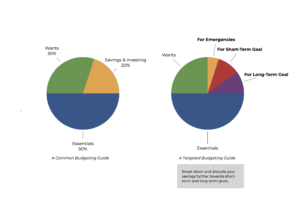

A common budgeting guide follows the 50/30/20 rule (see Fig. 1):

- 50% on essentials

- 30% on wants

- 20% on savings and investing

This isn’t a one-size-fits-all solution, but it’s a good benchmark to start evaluating your spending habits.

Fig. 1: A common budgeting guide.

3. Saving and Investing

Are you saving too little – or maybe even too much without growing it? Money sitting in a savings account may actually lose value over time due to inflation. That’s where investing comes in.

Just as regular workouts build physical strength, consistent saving and investing strengthen your financial well-being. Take advantage of the power of compounding and start early, it gives your money more time to grow and work for you.

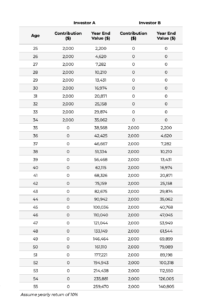

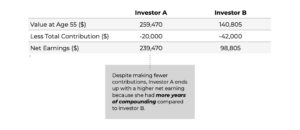

Example:

Let’s compare two individuals, Investor A and Investor B, both age 25 with a goal to retire at age 55.

Investor A begins investing early, contributing $2,000 annually for just 10 years – from age 25 to 34. After that, she makes no further contributions but leaves her investment to grow.

Investor B delays starting until age 35 but invests $2,000 annually for 21 years, continuing until age 55.

Here’s how their investment outcomes compare:

4. Monitoring and Evaluation

Financial planning is not a one-off exercise. Life changes, goals shift, markets move. Regular reviews keep your plan relevant and effective.

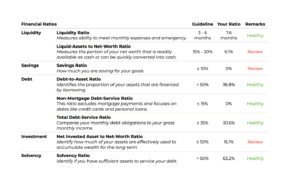

Financial ratios – similar to health screening reports, can give a snapshot to see where you stand.

Above sample report with Financial Ratio.

For example, Liquidity Ratio measures your ability to pay your bills and handle unexpected expenses without needing to sell other assets. A general emergency fund should cover 3 – 6 months of expenses. If your expenses are $2,500/month, aim to have about $15,000 in liquid savings.

The Savings Ratio is a simple way to see how much of your income you’re saving, not spending. A higher ratio means you’re saving a larger portion of your income, which is generally considered a good financial practice.

However, while saving a large portion of your income monthly seems healthy, it’s not ideal if all of it is in low-interest accounts. Consider asset allocation – based on your time horizon and risk appetite – to balance between short-term stability and long-term growth (See Fig. 1 above).

Schedule regular reviews with your trusted financial adviser to track progress. Think of it like a health check-up – without it, you might miss signs of trouble or opportunities for improvement.

Case Study

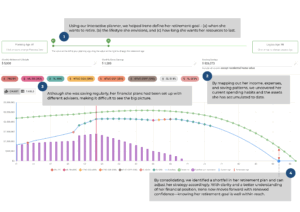

Using our interactive planner, we worked with Irene to assess her overall financial well-being, beginning with the fundamentals of Financial Management:

- Step 1: Setting Clear Financial Goals

Although Irene had a general desire to retire, we helped her define the specifics: When she wants to retire, what kind of lifestyle she envisions, and how long she would like her resources to last. - Step 2: Budgeting

By mapping out her income, expenses, and saving patterns, we uncovered her current spending habits and the assets she has accumulated to date. - Step 3: Saving and Investing

Irene had already embraced the power of compounding and had been investing at various stages of her life. Although she was saving regularly, her financial plans had been set up with different advisers, making it difficult to see the big picture. - Step 4: Monitoring and Evaluation

By consolidating everything, we gave her a clear, comprehensive view of her financial standing. This allowed us to identify a shortfall in her retirement plan and adjust her strategy accordingly.

With a clear roadmap and a better understanding of her financial position, Irene now moves forward with renewed confidence—knowing her retirement goal is well within reach.

Get Financially F.I.T.

Financial fitness doesn’t happen by chance, it happens by choice. Assess where you are, identify gaps, and take steps toward financial health. Just like physical fitness, it’s a journey that requires guidance, structure, and discipline.

If you’re unsure where to begin or want a professional diagnosis of your financial health, our Financially F.I.T. program is here to help. Reach out today and take the first step toward becoming financially fit.