Are you a retiree looking for dependable passive income? Or an investor who wants your investments to generate cash flow to cover monthly expenses? The “money laddering” strategy is a simple, structured way to achieve this goal by creating predictable, repeating cash flow.

View the CNA Money Mind: Cash Flow Generation using Laddering Strategy.

What is a Money Laddering Strategy?

Laddering is the process of splitting your total investment capital into smaller parts (or “rungs”). Instead of putting all your money into one asset that pays out once a year, you invest in multiple assets that mature or pay out at different, staggered times.

The Key Benefit: This ensures money flows into your bank account regularly, often monthly or quarterly, instead of waiting a full year or more for returns. This stable cash flow is valuable even when the market is flat or interest rates are falling.

You can build ladders using a mix of assets, including short-term bills, government bonds, Dividend ETFs, and REITs (Real Estate Investment Trusts). The goal is to choose your own risk level, from safe and slow to higher yielding options.

Case Study 1: The Retiree’s Safe Ladder (Lowest Risk)

This strategy prioritizes safety and liquidity above all else. It’s perfect for retirees or cautious investors whose primary goal is preserving capital while ensuring a fixed income stream.

The Strategy: Singapore Savings Bonds (SSBs) Mini-Ladder

A practical way to start small is to build a mini-ladder using Singapore Savings Bonds (SSBs).

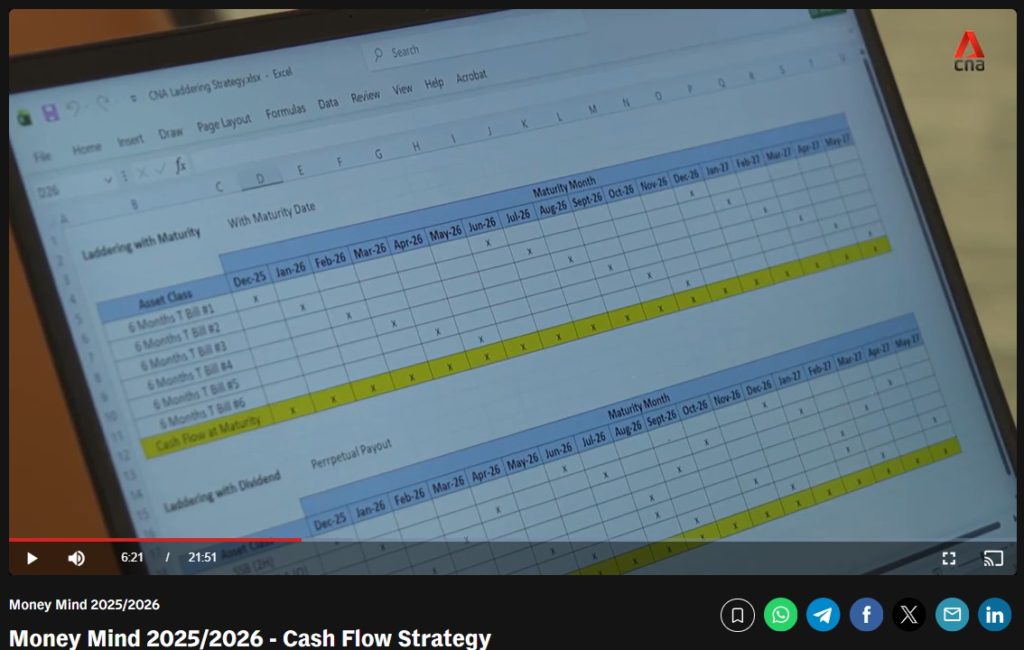

- How it works: SSBs pay interest every six months. By splitting a modest sum (e.g., S$1,000) and investing it across 12 different SSB issues over 12 consecutive months, you create an effective monthly payout schedule.

- Payout Start: You start receiving your first payout in Month 7. After that, a payout will arrive every month as the interest from each bond issue kicks in.

- Instruments & Risk: This ladder uses instruments with low risk and high liquidity:

- SSBs: Low risk, redeemable anytime with one month’s notice.

- Fixed Deposits (FDs): Low risk, but penalizes early withdrawal.

- T-bills (6M/1Y): Low risk, locked until maturity.

- Trade-off: The investment is simple, low maintenance, and government-backed, but the yield is generally low (e.g., around 1.33% for a recent 1-year rate).

Case Study 2: The Business Owner’s Balanced Ladder (Moderate Risk)

This strategy is suitable for investors or business owners who want to beat low fixed deposit rates and are comfortable taking on a little more market movement to potentially triple their yield.

The Strategy: Blending Stability with Market Exposure

The Balanced Ladder blends the stability of low-risk instruments with moderate exposure to income-paying listed assets.

- How it works: It combines fixed-income assets with growth assets to achieve a higher, but still stable, return. A typical 60/40 allocation (60% fixed income, 40% growth) can yield around 3.5%.

- Instruments & Risk:

- Low Risk (For Stability): SSBs and T-bills (6 months to 10 years).

- Medium Risk (For Moderate Yield): Corporate Bonds (2-5 years) and SGS Bonds (Singapore Government Securities).

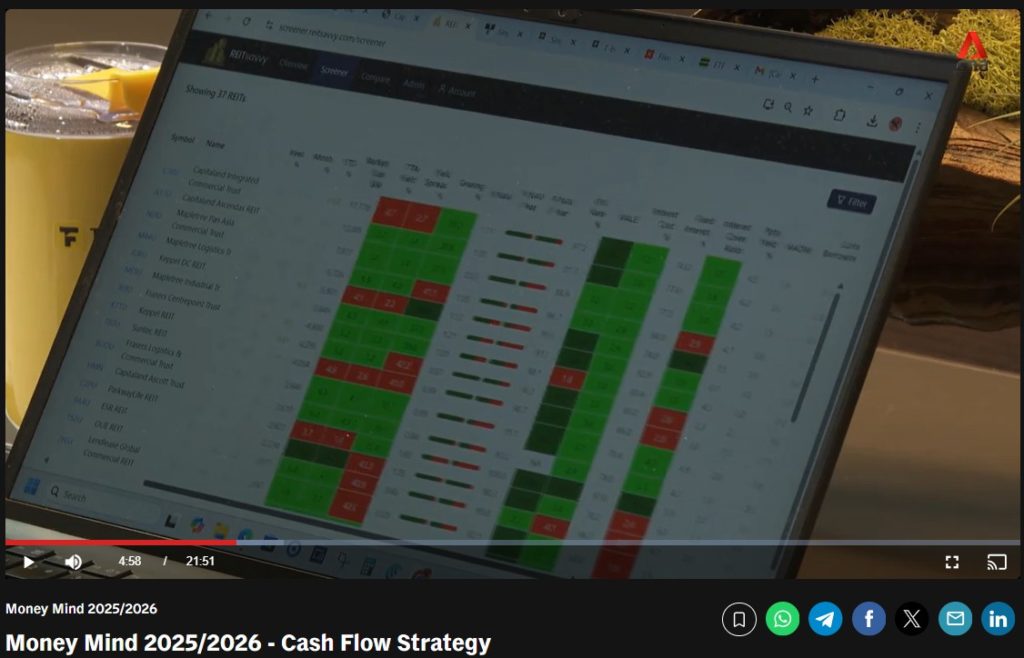

- Medium Risk (For Income/Growth): Dividend ETFs and REITs (listed, open-ended).

- Purpose: Short-term bills ensure steady cash flow and liquidity; bond funds provide stability; and REITs/ETFs offer potential capital growth and higher income. The idea is to balance safety and growth.

Case Study 3: The Active Investor’s Dividend Ladder (Higher Income)

This strategy is for investors who are comfortable with volatility and want to maximize monthly cash flow from their portfolio to pay for monthly expenses.

The Strategy: Targeting High-Yield Payouts

This ladder uses high-yielding, income-focused assets that are planned to pay out at different times throughout the year.

- How it works: By tracking the payout dates of different assets, you can set up a rhythm to receive cash flow almost every month. A 5% yield on a S$50,000 portfolio can generate about S$2,500 a year.

- Instruments & Risk:

- High Risk (For Yield): REITs and High-Dividend Stocks (open-ended).

- Medium-High Risk (For Support): Bond ETFs and higher-rated Corporate Bonds (1-5 years).

- Important Note: While payouts can grow as companies raise dividends, you must remember that companies can pause or cut dividends. Consistency and stability of the underlying business matter as much as the headline yield.

🔑 The Discipline of Laddering

No matter which ladder you choose, discipline is key.

- Reinvesting is Crucial: When an asset matures (e.g., a 6-month T-bill), you must roll it over (reinvest it) into the next cycle. Skipping this step breaks the rhythm of your cash flow.

- Tracking: Many investors automate this process by setting up a spreadsheet or using reminders to track maturity dates and reapplication windows.

- Market Opportunity: The continuous cash flow provides a major advantage: when there is a market correction, you have cash available to invest immediately at lower prices, helping you capture the upside later.

The goal of any money ladder is simple: to create a dependable, steady cash flow that you can count on, all while your money keeps working.