Buying insurance is often treated like a shopping trip, but it is more akin to building a structural foundation for a house. Without a blueprint, you end up with “spare parts”—policies that don’t fit together, leaving you over-insured in some areas and dangerously exposed in others.

For families with young children, the stakes are higher. This guide provides a holistic framework to move from “buying products” to “managing risks.”

1. The Risk Management Framework

Before looking at policies, you must decide how to handle different life risks. In professional risk management, we use four strategies:

-

Avoid: Steer clear of high-risk behaviors (e.g., extreme sports without training).

-

Reduce: Mitigate the impact (e.g., regular health check-ups, installing smoke detectors).

-

Retain: Self-insure for small losses (e.g., a broken smartphone or a common cold).

-

Transfer: Shift large, catastrophic risks to an insurance company (e.g., Critical Illness, Death).

The Rule of Thumb: Only transfer risks that you cannot afford to pay out of pocket. If a $2,000 dental bill won’t ruin you, but a $2,000,000 cancer bill will, focus your premium dollars on the latter.

2. Needs-Based Analysis (The “DIME” Method)

To stop guessing your “Sum Assured” (the payout amount), use the DIME formula. This identifies the capital your family needs if you were no longer around to provide.

The Formula:

* Subtract your current savings and existing CPF/insurance to find your “Protection Gap.

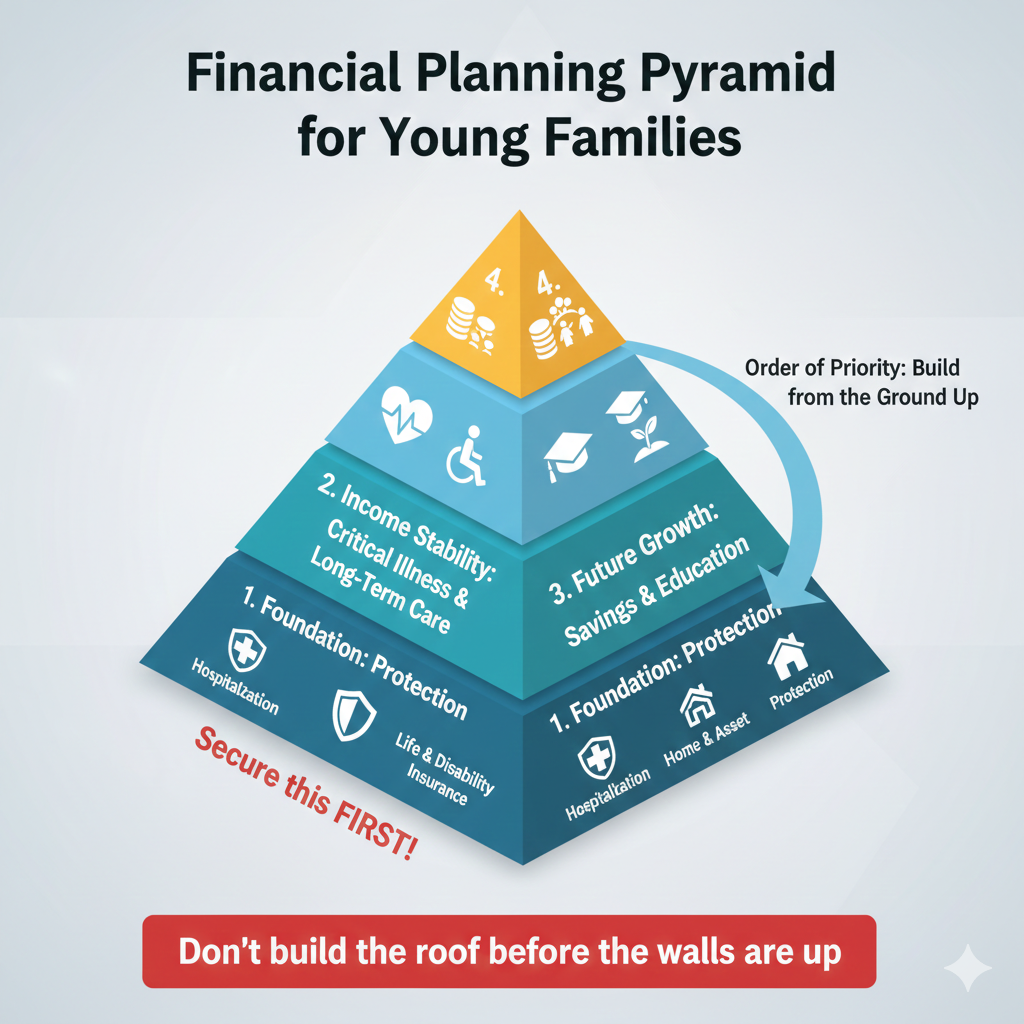

3. The Insurance Pyramid (Order of Priority)

For a family with young children, you must build from the bottom up. Do not buy an “Education Fund” (top) if you haven’t secured “Hospitalization” (bottom).

-

Hospitalization (Medical): The most frequent risk. Ensure you have an Integrated Shield Plan (or equivalent) to cover large hospital bills.

-

Critical Illness (CI): This replaces your income while you are alive but unable to work due to illness.

-

Life Insurance (Death/TPD): Provides a lump sum for your dependents (The “DIME” amount).

-

Wealth Accumulation: Education funds or retirement plans.

4. Comparing Insurance Types

| Type | Best For… | Pros | Cons |

| Term Life | Pure Protection. Families needing high coverage on a tight budget. | Lowest cost for the highest payout; straightforward. | No cash value; coverage ends after the term (e.g., at age 65). |

| Whole Life | Lifelong legacy. Those who want “forced savings” + permanent cover. | Covers you forever; builds cash value; premiums are usually fixed. | Much more expensive than Term; lower coverage for the same dollar. |

| Investment-Linked (ILP) | Flexibility. Those comfortable with market volatility. | Can increase/decrease coverage; potential for high returns. | Investment risk is yours; “Cost of Insurance” rises as you age, potentially eating the value. |

5. Checklist for Families

-

Insure the “Golden Goose” first: Many parents buy plans for the baby but neglect themselves. If the parent (the income earner) is not insured, the baby’s plan may lapse if the parent can no longer pay premiums.

-

Check for “Payer Benefit” Riders: Ensure the child’s policies have a rider that waives future premiums if the parent passes away or becomes disabled.

-

Avoid “Double Counting”: If your company provides $200k life insurance, you only need to buy the remaining gap from your DIME calculation.

Summary of Key Principles

-

Risk Management Strategy: Move from simply “buying” to strategically managing risks by Avoiding, Reducing, Retaining, or Transferring them to an insurer.

-

The DIME Method: Use a data-driven approach to calculate your protection gap by totaling Debt, Income replacement, Mortgage, and Education costs.

-

The Priority Pyramid: Build your foundation from the ground up—prioritize Hospitalization and Income Protection before moving to wealth accumulation and education savings.

-

Choosing the Right Tool: Select insurance based on specific needs: Term for high-cost protection, Whole Life for permanent legacy, or ILPs for investment flexibility.

Stop Buying Policies. Start Building a Plan.

Don’t leave your family’s future to chance or a collection of mismatched policies. A holistic plan ensures you are never under-insured during a crisis or over-paying for coverage you don’t need.

Ready to secure your family’s foundation?

[Click CONTACT ME below to Start Your Personalized Needs-Based Analysis]