When we hear the term “estate planning,” most of us think of one thing: writing a Will. It’s a vital first step, certainly. But viewing a Will as the entirety of your estate plan is like bringing only an umbrella to a hurricane. It might help in one specific kind of weather, but it won’t protect you from the flood, the wind, or the power outage.

True estate planning isn’t about a single document; it is about creating a comprehensive, resilient structure designed to address the multifaceted reality of life’s “what-ifs.” This is especially critical once you pass age 40, a time when family responsibilities are often highest, assets have grown more complex, and the risks of health crises become more tangible.

The objective is clear: to ensure your family is protected in every conceivable life state. To achieve this, you must move beyond simple asset distribution and embrace a structure that proactively manages different scenarios.

Understanding the Three Life States

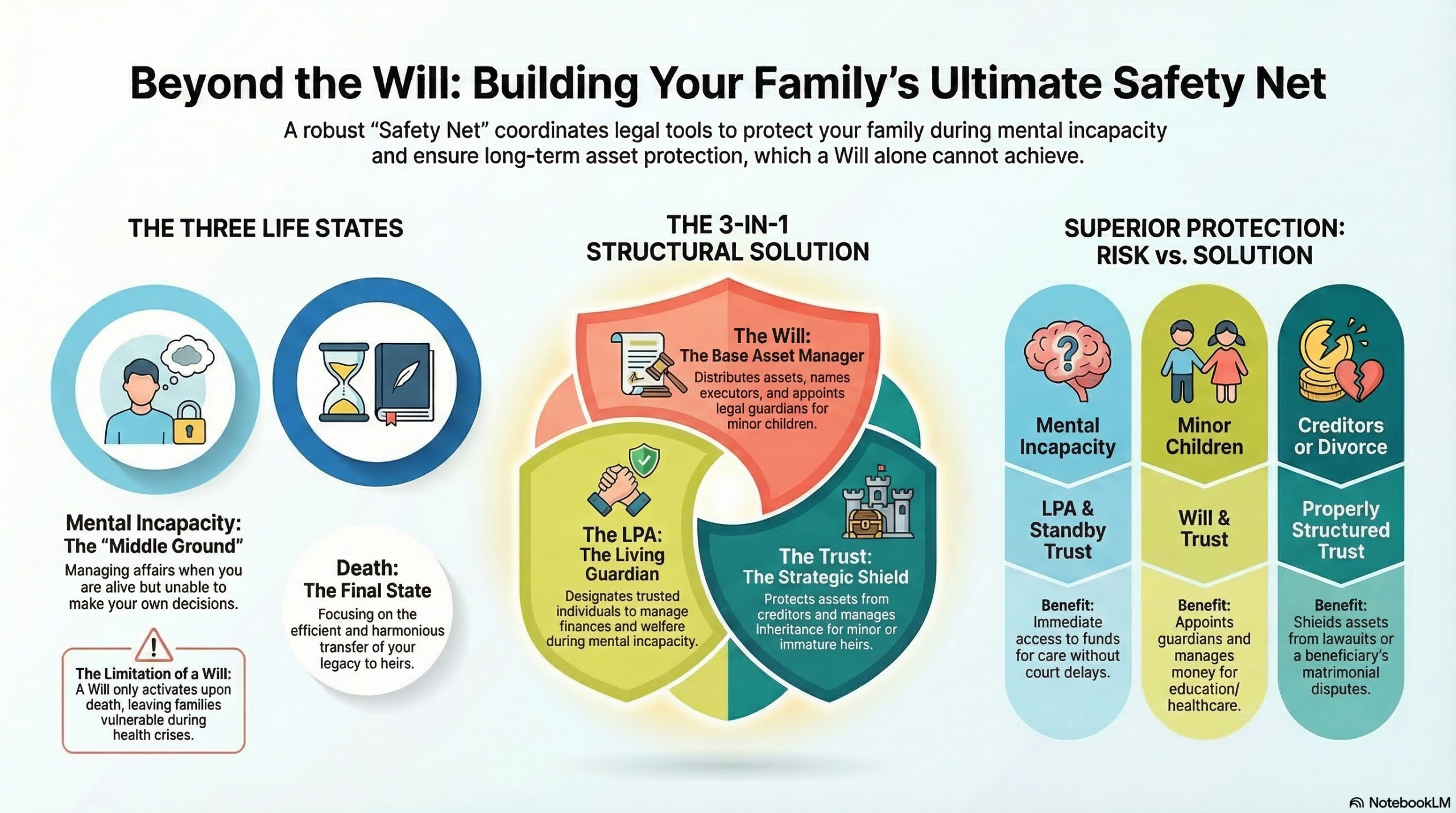

To appreciate the need for a robust structure, we must first recognize that estate planning addresses more than just death. It must manage your affairs across three distinct scenarios:

-

Good Health: This is where you are now—active, capable, and in control. The goal here is organization and laying the groundwork for the future.

-

Mental Incapacity: This is the oft-ignored middle ground. Due to accident, illness, or age, you may become alive but unable to make your own decisions. Without a plan, your family faces a legal nightmare just to pay your bills or make medical choices for you.

-

Death: The final state. The focus here shifts to the efficient, harmonious transfer of your legacy to the next generation.

The Anatomy of a Proper Estate Planning Structure

A simple Will only addresses the third scenario (Death). A proper estate planning structure coordinates multiple tools, each designed to excel in different scenarios while complementing the others.

The Role of a Will: The Base Asset Manager

A Will is the cornerstone of distribution. It specifies who gets what assets, points a finger at who will be in charge (the Executor), and—most critically for parents—appoints guardians for minor children. It provides clarity and prevents your estate from falling into the rigid, one-size-fits-all rules of government intestacy law.

The Role of an LPA: The Living Guardian

The Lasting Power of Attorney (LPA) is perhaps the most critical component while you are alive. It bridges the gap during mental incapacity. It allows you to appoint trusted individuals (Donees) to manage your property, finances, and personal welfare if you lose the ability to do so yourself. Without an LPA, your family may have to apply to court for deputyship—a costly, lengthy, and distressing process.

The Role of a Trust: The Ultimate Strategy and Protection Tool

A Trust adds a layer of sophistication, protection, and flexibility that a Will cannot match. By transferring assets to a Trust, they are managed by Trustees for your chosen beneficiaries. This provides several powerful scenario-based advantages:

-

Scenario: Spendthrift Heirs. Instead of giving a large lump sum to a financially immature beneficiary, a Trust can distribute income gradually, ensuring the inheritance lasts.

-

Scenario: Minor Children. A Will can nominate guardians, but a Trust manages the money precisely for the child’s maintenance, education, and healthcare until they reach a responsible age.

-

Scenario: Creditor/Divorce Protection. Properly structured Trusts can shield assets from potential lawsuits, business creditors, or a beneficiary’s matrimonial disputes.

-

Scenario: Mental Incapacity. Unlike a Will, which only activates upon death, a standby trust can immediately activate upon incapacity, allowing Trustees to use assets for your care without legal delays.

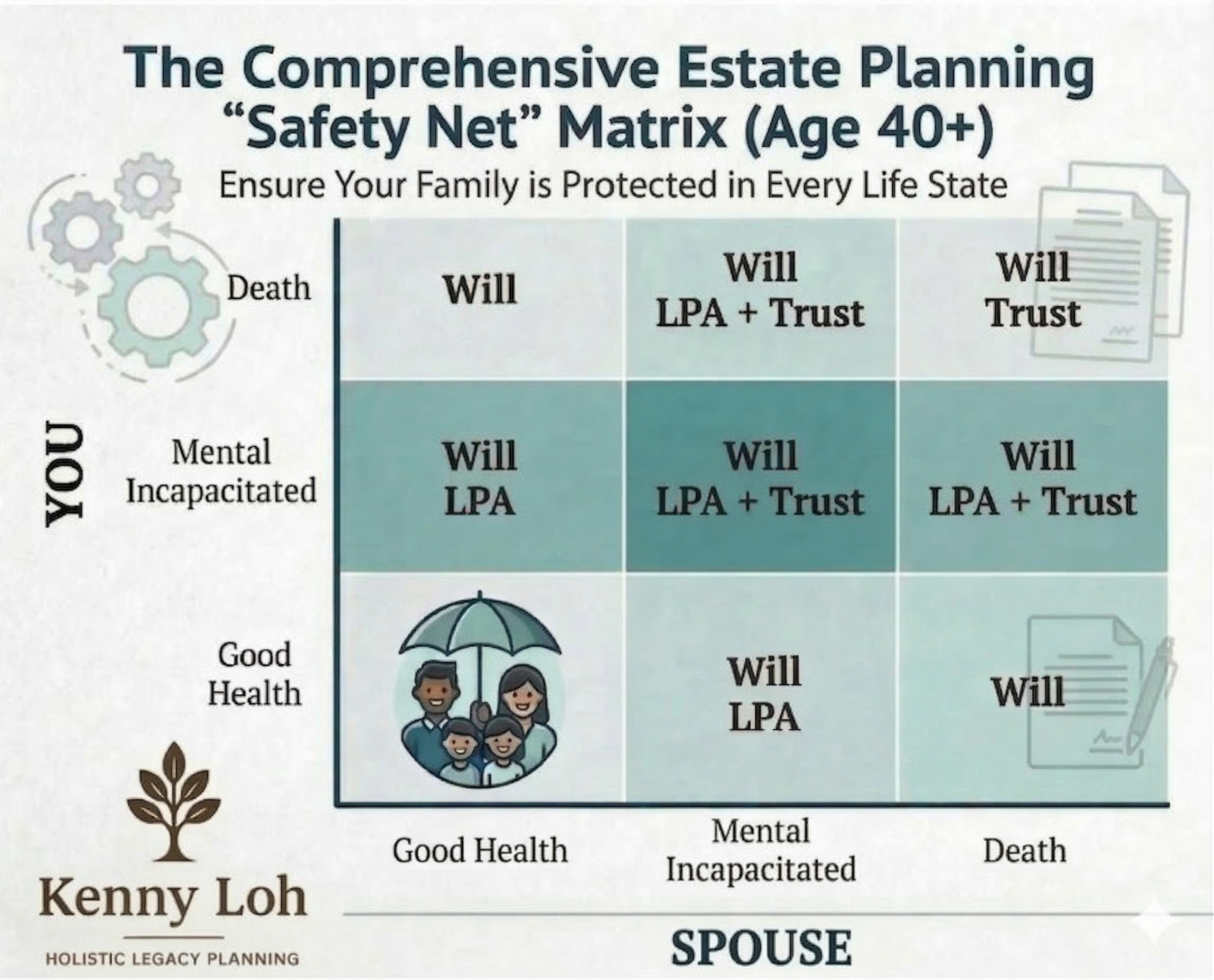

Scenario Matrix: Putting the Structure to the Test

To maximize clarity, consider how these different tools interact to protect a family, such as a married couple (“Me” and “Spouse”).

-

Scenario 1: Both “Me” and “Spouse” are in Good Health.

-

Need: The baseline plan is set up, organized, and reviewed annually. Assets are nominated correctly (CPF, Insurance), and the structure is “active status,” ready for any shift.

-

-

Scenario 2: “Me” becomes Mentally Incapacitated.

-

Need: Immediate management of medical care and bills.

-

Structured Solution: My LPA activates. My designated Donee takes control of finances. If a Trust exists, Trustees can also deploy funds for my maintenance. My Will remains inactive.

-

-

Scenario 3: “Me” Dies.

-

Need: Efficient transfer of assets, care for minor children, support for surviving spouse.

-

Structured Solution: My Will activates. CPF and Insurance pay out directly to nominees. Jointly held property passes to the spouse. If I have young children, guardians are appointed via the Will, and assets might flow into a Testamentary Trust for their managed support.

-

-

Scenario 4: The Complex Scenario (Concurrent Events).

-

Example: “Me” becomes mentally incapacitated, and subsequently, “Spouse” dies.

-

Need: Who is managing the incapacitated person’s care while also managing the deceased spouse’s estate?

-

Structured Solution: This requires a robust structure. “Me” has an active LPA with backup donees. “Spouse” had a Will & Testamentary Trust, providing managed income to support “Me” and their children, overseen by reliable Trustees.

-

The Dangers of “Just a Will”

Failing to set up this broader structure leaves gaping holes:

-

No Protection in Incapacity: A Will provides zero guidance or authority if you are alive but incapacitated.

-

Inflexibility: A Will is rigid. It generally provides lump-sum distributions, which may not suit vulnerable or immature beneficiaries.

-

Probate Delays: A Will must go through probate—a court process that can take months, freezing assets when your family needs them most. Trusts can often bypass probate entirely.

-

No Creditor Shield: Assets distributed via a Will become the beneficiary’s property, making them vulnerable to creditors or divorce settlements.

Take Action: It’s Time to Structure Your Legacy

Estate planning is not a morbid task to be feared; it is an act of profound love and responsibility. It is the ultimate gift of certainty and harmony to those you care about.

Delaying your planning is simply planning to delay your family’s security. A comprehensive structure minimizes the potential for family disputes, speeds up wealth transfer, avoids unnecessary legal costs, and protects you and your assets while you are alive.

Do not settle for just an umbrella. Work with qualified estate planning professionals—lawyers, financial advisors, and trust experts—to build a multi-layered, resilient “Safety Net” structure that guarantees your family is truly protected, in every life state, for generations to come.

Start today. Your family is worth it.